Suzhou International Science and Technology Park Industry Sharing Session

Suzhou International Science and Technology Park Industry Sharing Session

1 month12Today, Suzhou International Science Park, in collaboration with Frost & Sullivan, a leading consulting firm in the industryFrost & SullivanThe industry sharing event jointly organized by Frost & Sullivan and LeadLeo Research Institute, referred to below as 'Frost & Sullivan', was successfully held at the Artificial Intelligence Industrial Park.

This sharing session will focus on four major artificial intelligence sub-industries: integrated circuits, machine vision, industrial software, and optical communications. Dr. Wang Xin, a global partner at Frost & Sullivan, President of Greater China, Founder and Chairman of LeadLeo, and Founder of YUAN CAPITAL, will serve as the keynote speaker.

At the beginning of his speech, Dr. Wang Xin stated,2022The year is a historic one for the semiconductor industry, looking back2022In [year], the semiconductor boom is over, market conditions began to decline, and global semiconductor sales growth slowed significantly in the second half of this year. A cyclical market is expected to continue until2023The market will rebound in the second half of the year.

At the beginning of his speech, Dr. Wang Xin stated,2022The year is a historic one for the semiconductor industry, looking back2022In [year], the semiconductor boom is over, market conditions began to decline, and global semiconductor sales growth slowed significantly in the second half of this year. A cyclical market is expected to continue until2023The market will rebound in the second half of the year.

In addition, the ongoing tensions between the US and China continue to affect the global supply chain, and the development prospects of China's semiconductor industry are fraught with many uncertainties. As a result, the path for China's semiconductor industry remains long and snowy. This sharing session will delve into the development history of China's semiconductor industry, as well as explore the future opportunities and challenges of the industry.

Global Partner and President of Greater China at Frost & Sullivan, Founder and Chairman of LeadLeo, and Founder of YUAN CAPITAL Dr. Wang Xin

Dr. Wang Xin pointed out that the importance of the Chinese market to the global semiconductor industry is self-evident.

As of now, the Asia-Pacific region remains the largest regional semiconductor market, with China being the largest market in the region, accounting for56%Global markets35%, that is to say, China consumed about35%semiconductor products. However, Chinese local semiconductor companies only provide for the global7.6%Semiconductor products, with their significant consumption and supply gap, have forced China to import a large amount of these products. The proportion of China's semiconductor imports in the industry's output value is also continuously increasing.2010year11.24%, to2015year13.69%, and then to2020year16.97%, This also means that China's dependence on overseas semiconductor products is constantly increasing.

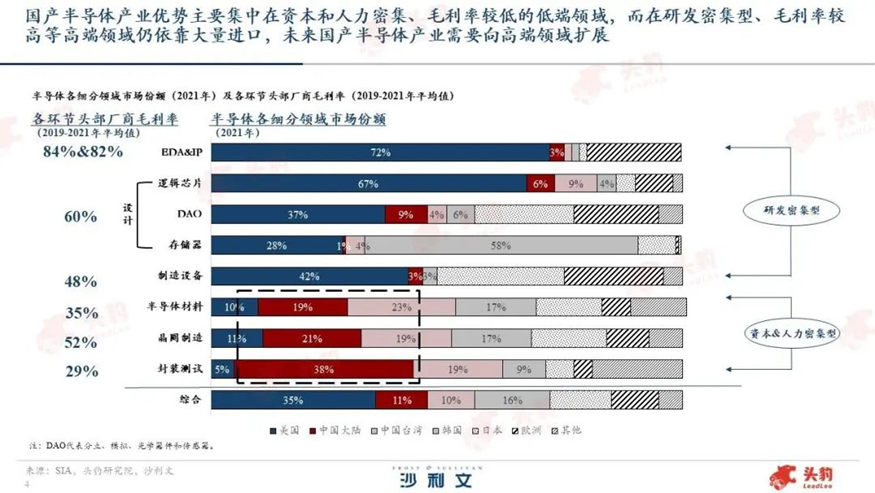

First is in terms of market share by sub-sectors , From the market share of various sub-sectors within semiconductors, it can be seen that the current advantages of the domestic semiconductor industry are mainly concentrated in capital- and labor-intensive areas such as semiconductor materials, wafer manufacturing, and packaging testing. In the research and development-intensive sub-sectors, such as semiconductor design softwareEDA,IP addressWait, Chinese semiconductor companies have performed weakly.

Observing the gross profit margins of leading companies in various segments, the gross profit margins of upstream support sectors are generally higher, especially those with light assets.EDA,IP addressIn the authorization process, the gross profit margin is as high as84%,82%Design manufacturers benefit from the highly vertical division of labor across all links of the industrial chain, adoptingFabless InteractiveModel, hence the gross profit margin is maintained at a relatively high level60%At the same level, wafer manufacturing also has considerable gross profit due to technical barriers of advanced processes.52%At a certain level, the beta testing phase is located in the mid-to-late stages of the industrial chain, with poor bargaining power. The gross profit margin is about29%That is to say, A large number of domestic semiconductor companies are still concentrated in sectors with low gross profit margins and weak R&D efforts. In several key, R&D-intensive, high-gross-profit-margin sub-sectors, there is still a long-term need for substantial imports from overseas. , The core links are controlled by other countries, putting the industrial chain in a passive position. In the future, the domestic semiconductor industry needs to expand into high-end fields.

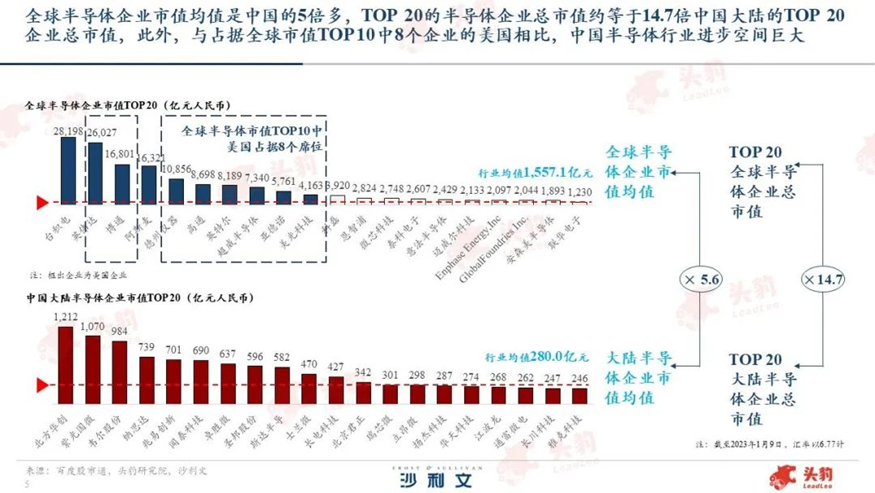

From the perspective of enterprise market value , As of1month9Today, TSMC, NVIDIA, Broadcom, and ASML rank among the top four in global semiconductor market value, all with a market value exceeding1.6Trillion yuan. The market values of China's northern companies, Huachuang Technology and Unigroup Microelectronics Corporation (UVIC), both exceed one trillion yuan, ranking among the highest market values of semiconductor enterprises in ChinaTop 2.

Overall, the market value of semiconductors in Mainland China lags far behind global markets The global semiconductor industry average has reached1,557.1100 million yuan, while the average in the Chinese mainland semiconductor industry is only280yuan, with a gap of about5times The market value of NVIDIA alone is approximately equal to that of the Chinese mainlandTop 20The sum of market values of semiconductor companies2.4times, Top 20The global semiconductor market value is approximately equal to14.7Double that of the Chinese mainlandTop 20The sum of the market values of semiconductors , The huge market value gap also shows that China's semiconductor industry still has significant room for progress.

In addition, as of1month9market valueTop 10In, U.S.-based companies dominate8The seat holds a clear advantage, and the Chinese mainland has not yet made it into the top ten, let alone the top twenty. The Chinese mainland has not yet cultivated world-leading semiconductor giants.

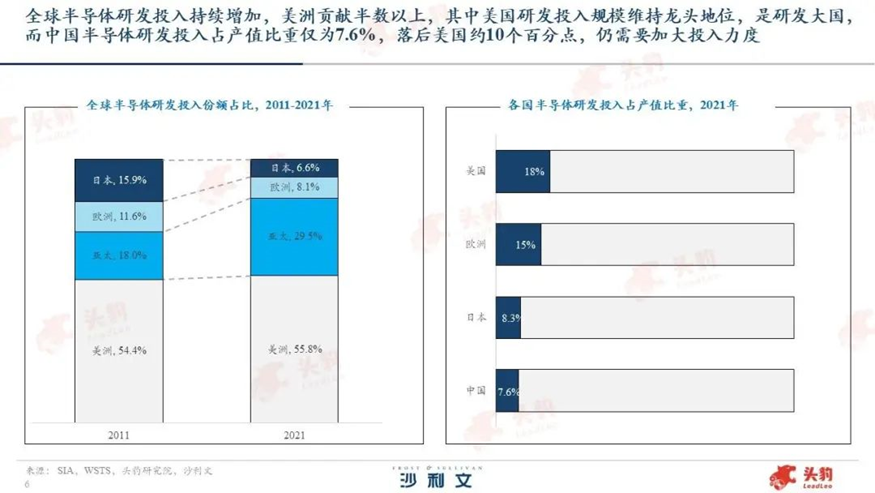

Judging from R&D investment , As of2021The global semiconductor R&D investment has reached80.5billion US dollars, compared to2011year50.8billions, growth58.5%There has been a significant increase, with R&D investment in the Americas maintaining a strong upward trend. The proportion of R&D investment has changed from2011year54.4%expanded to2021year55.8%, improve near1.4percentage points Contribute more than half, among which the United States maintains its leading position in R&D investment scale and is a research powerhouse.

Looking at the intensity of semiconductor R&D investment in various countries, the R&D investment in the US and Europe remains relatively strong, with the proportion of R&D investment to output value in both regions being10%Above, While China's proportion is only7.6%lagging behind the United States by about10Percentage points indicate that China's investment in semiconductor research and development is insufficient, and more investment is still needed.

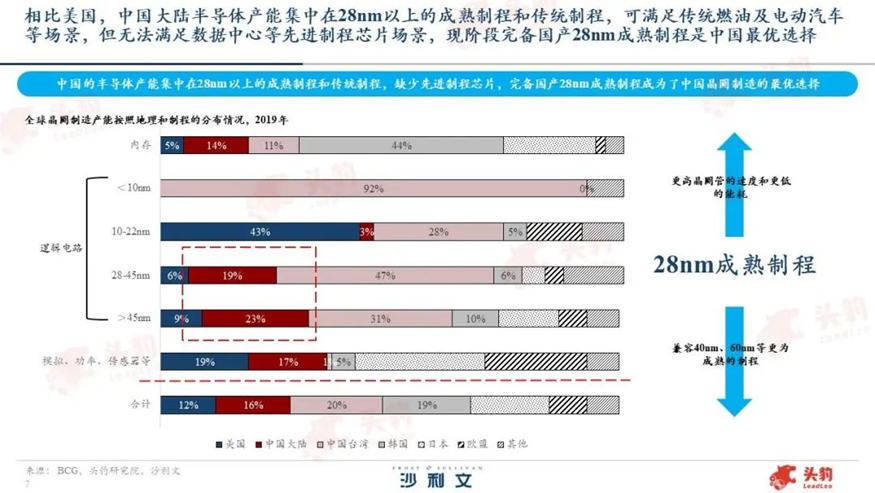

In terms of mass production processes, Semiconductor process with28nmAs a demarcation line, it is divided into advanced processes and mature processes. In terms of demand, the demand for advanced processes is increasing year by year, while the demand for mature processes is relatively stable. China's semiconductor production capacity is mainly concentrated in28nmThe current process level of SMIC can reach up to the above mature and traditional processes14nm, but mainly still focused on production28nmMainly chips above this level, and Hua Hong Semiconductor is also2020Announced that the process has reached14nmHowever, the yield ratio only exceeded25%.

Finally, From the perspective of application scenarios, China's semiconductor production capacity can meet the development needs of traditional fuel vehicles, electric vehicles, electric drives, etc., but it cannot satisfy the demands of high-end consumer electronics, data centers, and other scenarios that require advanced process chips. This also means that China is still very far from achieving 'high-end manufacturing'.

Dr. Wang Xin believes that, under the pressure of semiconductor technology and processes, complete domestic28nmThe mature process has become the optimal choice for China's wafer manufacturing. Everyone sees it in the news every day10 nm,7nm,5nmThe chip, but its application range is actually very narrow, exceptCPU,GPU,AIExcept for products with high requirements for performance-to-power ratio such as acceleration, most consumer electronics used in daily life, such as smartwatches, mid- to low-end tablets, TVs, air conditioners, industrial chips, etc.,28nmThe process can fully meet the requirements. With the increasing market demand for terminal products such as tablet computers, wearable devices, and smart home appliances, it is predicted28nmProcess platform in the future10There is a huge market demand every year.

Technically,28nmThe manufacturing processes and production equipment used in the process can be compatible.40nm,60nmWaiting for a more mature process means that even if businesses expand28nmThe production line of the process, when28nmWhen the capacity demand declines, these devices can also be put into production of more mature processes. In addition28nmIt brings higher transistor speed and lower energy consumption, and40nmIn comparison,28nmGate density transistor speed is improved by about50%, energy consumption has been reduced50%.

However, In the field of semiconductor manufacturing, China's most mature level is at28nm, mainly centered around MediaTek International and Shanghai Huahong in the headquarter region, although they can complete28nmThe process has been mass-produced, but the full localization of the industrial chain has not been completed. The backward links are mainly in key equipment and materials, which are still domestically produced.28nmThe semiconductor self-sufficiency rate is still insufficient20%.

Therefore, Dr. Wang Xin emphasizes that choice28nmThe mature process is a strategic step for China's semiconductor industry to break through the 'bottleneck' of chip supply.

Dr. Wang Xin also stated that although there are some shortcomings in China's semiconductor industry, it cannot be ignored that the industry has delivered impressive growth rates and has gradually developed its own characteristics and highlights.

Semiconductor market sizeCAGRLook, China2005 - 2013Annual semiconductor market sizeCAGRfor13.1%Japan's growth was negative,2013 - 2021yearCAGRfor9.5%, Japan: This data is only2.9%The market scale of semiconductors in ChinaCAGRThe performance is remarkable, reflecting the strong resilience of China's semiconductor industry development, showing a stable upward trend. At the same time, China's integrated circuit industry's share of the global industry2010year25.5%expanded to2021year34.6%Its international market share is growing larger and its output value contribution continues to increase.

As can be seen from the previous data, China's semiconductor industry has been on the rise and will continue to do so. Dr. Wang Xin believes that overall, there are three major highlights in China's semiconductor industry.

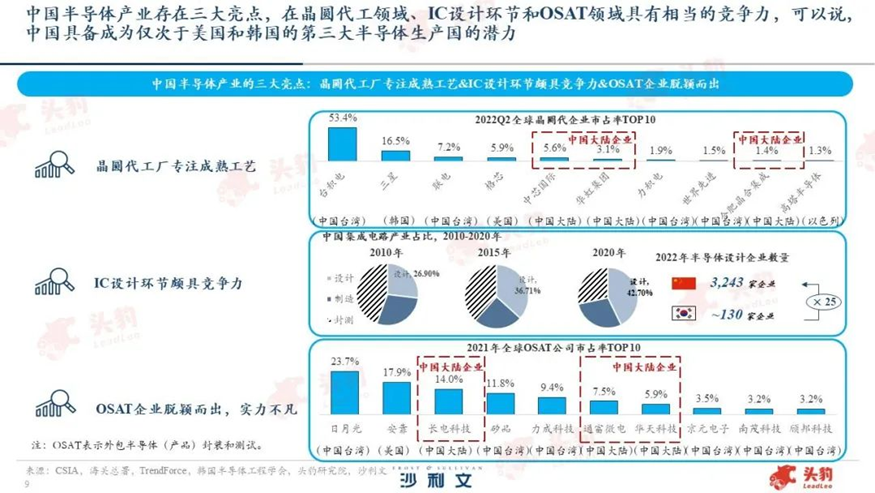

The first highlight is the mainland foundries' demonstrated advantages in mature processes. Market share of the world's top ten wafer foundriesTop 10Among them, mainland Chinese enterprises accounted for3The seats are occupied by SMIC International, Hua Hong Semiconductor, and Hefei Jinghe Integration respectively. The combined market share of these three companies exceeds10%The obvious advantage of Chinese OEM enterprises is their focus on mature processes, laying a solid foundation for their future leadership in the OEM market.

The second highlight is the Chinese mainlandICThe design phase is highly competitive. From the perspective of industry proportionality, China is intensifying efforts to extend upstream in the industrial chain, aiming to make breakthroughsICBottlenecks in design,2020yearICThe proportion of design output value reached42.7%relatively2010Year-on-year increase of nearly15.8Percentage points, and it is precisely because of China's high emphasis,ICThe design industry is gradually replacing industries with lower added value.ICPre-release testing industry. In terms of the number of companies, there are approximately3,243Home semiconductor design company, South Korea only130Home, the gap between the two is25about double, and in ChinaICThe number of design companies is still growing continuously.

The third highlight is in the downstream process, on the Chinese mainlandOSATThe company also has considerable competitiveness , At the forefront globally10bigOSATwithin the company,3The companies come from the Chinese mainland, namely Changjiang Electronics Technology Co., Ltd., ranked third, Tongfu Microelectronics Co., Ltd., ranked sixth, and Huatian Technology Co., Ltd., ranked seventh. The combined share of these three companies is approximately27%, exceeding Naspers' global market share lead. These data indicate that the Chinese mainlandOSATThe enterprise has performed exceptionally well in global competition. It can be said that China has the potential to become the third-largest semiconductor producer after the United States and South Korea.

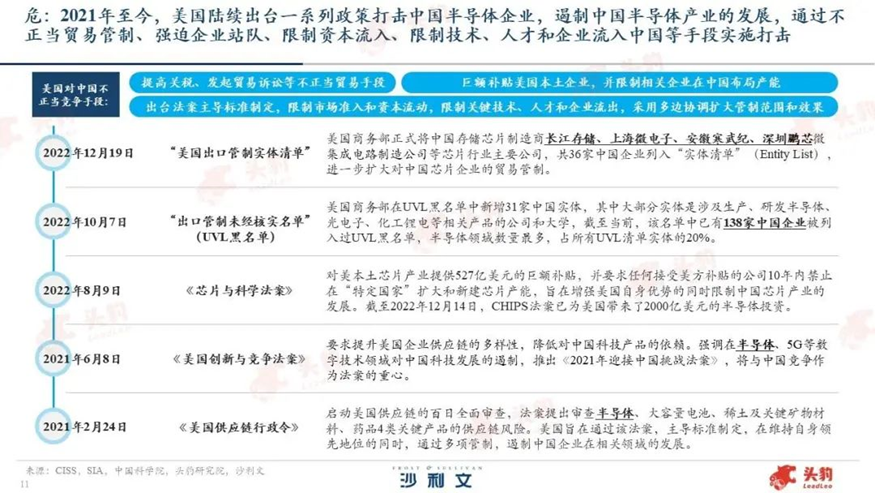

According to Dr. Wang Xin, as China becomes the world's largest semiconductor sales market, the supply chain risks in the US semiconductor industry are gradually increasing, leading to a series of US anti-Chinese policies.

China's semiconductor industry has become accustomed to rising against the odds amidst the pursuit and obstruction from the United States and its allies.2021Since the beginning of this year, the United States has successively introduced a series of policies towards China. Through various unfair trade controls, it has dominated capital flows, restricted technology, talent, and enterprise inflows into China, among other means, to combat Chinese semiconductor companies and contain the development of China's semiconductor industry in multiple aspects. At the same time, the United States has continuously called for strengthening multilateral cooperation with allies, aiming to impose more stringent export controls on China in order to gain competitive advantages. The international market is 'full of crises'.

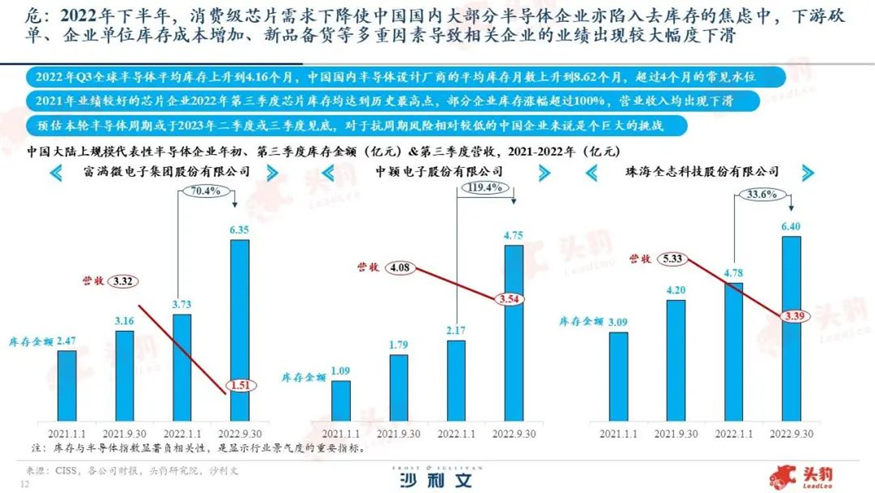

On the one hand,2022In the second half of the year, falling demand pushed most domestic enterprises into an anxiety about inventory reduction, and the industry entered a downward cycle. Multiple factors such as downstream order cancellations, RMB depreciation, increased unit inventory costs, and new product stocking have led to a significant decline in performance for related enterprises.

2022yearQ3 quarterThe average global semiconductor inventory month has risen to4.16months, with the average inventory months of domestic semiconductor design manufacturers rising to8.62months, exceeding the common3 - 4Inventory level for the next [X] months. International manufacturers such as Intel and Hynix, which mainly focus on consumer-grade chips, are also2022In the third quarter of the year, there was a significant decline in performance. In terms of Chinese enterprises,2021Chip companies with good annual performance2022In the third quarter of 2023, chip inventories reached their highest point in history, with some companies experiencing an increase in inventory exceeding100%Operating revenue has all declined.

Considering factors such as production ramp-up cycles and innovation cycles, Frost & Sullivan estimates that this semiconductor cycle may end in2023The bottom may be seen in the second or third quarter of next year. How to withstand this six-month period, especially against Chinese companies whose ability to counter cyclical risks is relatively weaker, poses a huge challenge.

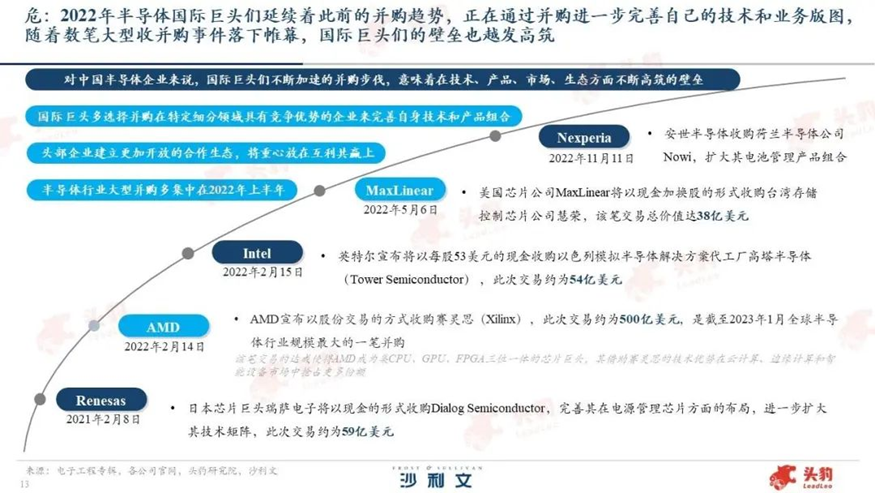

On the other hand,2022In [year], semiconductor international giants further improved their technology and business portfolios through mergers and acquisitions. By leveraging the resources and technological advantages of their acquirers, they better shaped their core competitiveness, consolidated their market position, and expanded into more potential markets.

However, for Chinese semiconductor companies, the accelerating pace of mergers and acquisitions by international giants means a widening gap in technology, products, market, and ecosystem. With several major acquisition events coming to an end, the barriers erected by international giants are becoming even higher. Giants use mergers and acquisitions to seize “CBit”, which not only preempts a company, some technology, or certain niche markets, but also potentially represents opportunities for domestic players. For some enterprises, survival in this gap will be even more difficult.

However, Dr. Wang Xin also firmly stated that, against the backdrop of a crisis-ridden environment, he is still optimistic about the Chinese semiconductor market for several reasons—simple as it is: 'There are people, there is a market.'

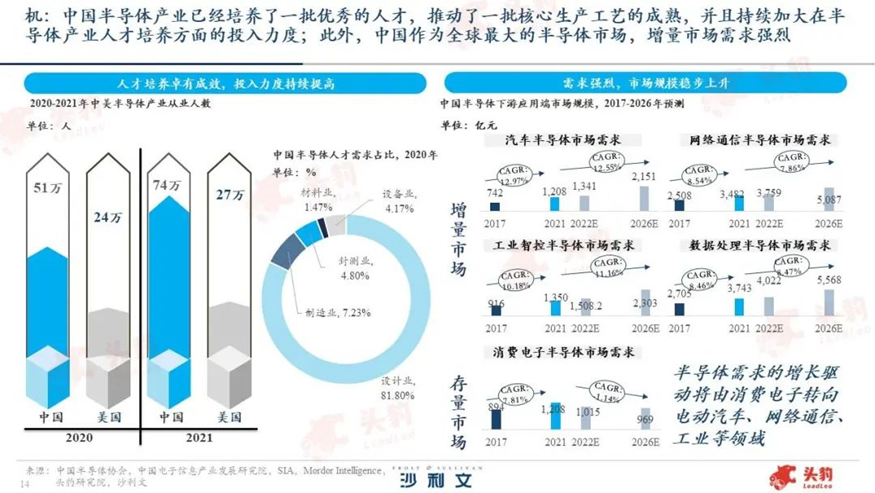

Semiconductors are the foundation of the electronic information industry and belong to an intellectual-intensive sector. They require a large investment in highly skilled professionals to achieve independent development and innovation in the semiconductor industry. China's semiconductor industry has now cultivated a group of outstanding talents and promoted the maturation of a number of core production processes, especially40nmThe above production process. Meanwhile, China is also continuously increasing its investment in talent cultivation for the semiconductor industry, especiallyICDesign phase.2021The number of employees in the US semiconductor industry reached27Ten thousand people, all increasing12.5%, and2021In China, the number of semiconductor industry practitioners reached74Ten thousand people, all increasing45.1%.

In addition, as the world's largest semiconductor market, China still has a strong demand. It can be seen that the main application markets for semiconductors include incremental markets such as automotive, network communication, industrial intelligent control, and data processing. China's growth rate over the next five years remains considerable. The consumer electronics market in the existing stock market is under pressure in the short term. Affected by multiple factors such as weak demand, high inventories, downstream cutbacks and price cuts,2022The annual consumer electronics market size is expected to shrink significantly and maintain a low growth rate for some time in the future. In the medium to long term, the growth driver of semiconductor demand will shift from consumer electronics to areas such as electric vehicles, network communications, and industry.

Among them, automotive semiconductors2021The annual market scale is1,2081000 million yuan, in the future5yearCAGRyes12.55%Network communication semiconductors2021The annual market scale is3,4821000 million yuan, in the future5yearCAGRyes7.86%Industrial intelligent control semiconductors2021The annual market scale is1,350.2100 million yuan, in the future5yearCAGRyes11.16%Consumer electronics semiconductors2021The annual market scale is1,2081000 million yuan, in the future5yearCAGRyes-1.14%; data processing semiconductors2021The annual market scale is3,742.51000 million yuan, in the future5yearCAGRyes8.47%It can be seen that the growth prospects of these segmented markets in China over the next five years remain highly certain.

In the medium to long term, the growth driver of semiconductor demand comes from mobile phones,PCConsumer electronics, represented by smartphones and tablets, are shifting towards electric vehicles, data centers, and new energy sectors. A new round of chip design innovation cycles and domestic substitution periods are expected to begin.

Dr. Wang Xin believes that in the future5 - 10In the year, the automotive industry, data center industry, and new energy industry are three of the most promising development areas, with overlapping sectors among them. The development of these three industries will grow at a high speed simultaneously, driving the rapid development of related integrated circuit chips.

Automobile industry: The rapid growth in new energy vehicle sales will effectively drive the development of integrated circuits. In addition, with the continuous development of connected and intelligent vehicles, the number of semiconductors required for automobiles will also double.

Data Center Industry: as5GWith the acceleration of business pace progress, the development of Internet of Things technology, and the expansion of applications such as online office work and metaverse in the post-pandemic era, data center servers will see increased demand and are expected to show a rapid growth trend in the future.

New Energy Industry: Energy shortage and in Under the 'dual carbon' goal, the development of new energy industries will continue to accelerate, thus putting photovoltaic inverters on fast track.IGBTThe demand for chips related to power management and other aspects will also multiply. On the other hand, this will promote the development of industrial automation, and the development speed of related power chips will accelerate.

With the further recovery of industry supply and demand, some industrial chain links such as chip design are expected to bottom out first and see a recovery in the second half of the year.

Dr. Wang Xin pointed out that by analyzing the entire integrated circuit industry chain from three different dimensions: market scale, industrial driving force, and localization progress, it is evident that the markets for integrated circuit design and packaging and testing are in high prosperity. In the future, it is expected to achieve rapid development driven by national policies and market demand.

In terms of the number of integrated circuit design enterprises, the integrated circuit design industry is currently in the industry's growth phase. This stage has two relatively prominent characteristics:

1.Flowers bloom everywhere, with local breakthroughs: Numerous technology innovation companies have emerged in niche areas;

2.Release the cleaning card for optimized resource allocation: Large enterprises have started mergers and acquisitions, with products, talent, and technology gradually converging.

Dr. Wang Xin believes that2025The year is a turning point for the integrated circuit design industry.2025After the Spring Festival, the number of integrated circuit design enterprises will tend to stabilize. Larger enterprises will acquire smaller ones in the industry, forming a concentration of technology, talent, and industry resources. The industry concentration will further increase, effectively reducing industry costs, achieving breakthroughs in core technologies, and further expanding market size.

From the perspective of domestic substitution , Some integrated circuit design companies in China have initially developed global competitiveness in their niche areas, and some have already achieved a high level of substitution capability. In the future3 - 5In [year], there is hope for gradual localization substitution in high-tech barrier areas.

Logic of integrated circuits in ChinaICsimulationICIn fields such as discrete devices, many enterprises with globally advanced technology levels have emerged, such as HiSilicon (mobile baseband chips), Zhaosheng Microelectronics (discrete RF switches and low noise components), HMD Technology (fingerprint recognition chips), and Lixin Semiconductor (low-power IoT chips).

3During the year, Chinese integrated circuit design companies required in the consumer electronics application fieldWIFI/Bluetooth chip,CIS,MCUPower management, optical chips, and some mid- to low-end memory chips already possess a high degree of substitution capability, and related integrated circuit design companies will also accelerate their growth.

In the long run, the future3 - 5In 2023, with the support of industry, academia, and research institutions, coupled with strong market demand, the growth trend of integrated circuit design capabilities in China remains unchanged. The high-end chip design capability has been significantly improved, and the development of radio frequency front-end transmitters with high technical barriers will gradually be realized./Receiving module, various types of memory chipsNAND gate,DRAM,nor),MEMSThe localization and substitution of sensors, etc., will also benefit related integrated circuit design enterprises, accelerating their development process.

computerMPU,FPGA, Customization for Vehicles/Standardized chips, for serversMPUandGPUThese technologies have high technical thresholds, core technologies are controlled by international giants, and coupled with the impact of the Sino-US trade war, the localization progress in these fields is almost0However, with the support of national policies, in the future10year10After the New Year, there are hopes for technological breakthroughs in these areas and the completion of domestic substitution.

Subsequently, Dr. Wang Xin briefly introduced the integrated circuit industry in Suzhou Industrial Park to everyone.

Firstly, the park has excellent locational advantages, with a solid foundation in integrated circuit industries in both Jiangsu Province and Suzhou City. . Jiangsu Province is located in the hinterland of the Yangtze River Delta and is one of the regions in China with an early start, solid foundation, and rapid development in integrated circuit industry. It holds a pivotal position in China's integrated circuit industry. According to data disclosed by the National Bureau of Statistics,2021The annual integrated circuit output of Jiangsu Province is118100 billion yuan, ranking first in the country, year-on-year2020Year-on-year growth42.1%, accounting for national output33%From the perspective of the industrial chain, Jiangsu Province has formed a coverage that includesEDAA relatively complete integrated circuit industry chain, including design, manufacturing, packaging, equipment, materials, etc., has gathered numerous well-known integrated circuit enterprises.

2021In 2023, the integrated circuit industry scale in Jiangsu Province reached3,440yuan, due to5GThe demand for integrated circuits in big data centers, cloud computing servers, tablets, automobiles, etc., continues to climb, and it is expected that in the future5The scale of the integrated circuit industry in Jiangsu Province will remain within18%The high-speed growth trend,2026The annual industrial scale will reach7,869.9100 million yuan.

Suzhou ranks second in the province in terms of integrated circuit scale, having introduced Infineon, Freescale Semiconductor,AMDA series of international big names, after years of development, Suzhou has formed an ecosystem centered around 'design-Wafer manufacturing-Focused on 'Package Testing', the integrated circuit industry chain supported by the equipment, raw materials and service industries, andMEMSThe region has a good industrial foundation in characteristic niche areas such as compound semiconductors and optical communications. It is one of the regions in China with a relatively complete industrial chain, high enterprise concentration, and leading talent reserves and technology development levels.2021In [year], the scale of Suzhou's integrated circuit industry reached606Yuan billion, expected in the future5In 2023, the scale of Suzhou's integrated circuit industry will still maintain a steady growth trend.

The competition within the province is fierce, Wuxi2021The annual industrial scale is1,780Rising to the second place nationwide with a value of hundreds of millions, it has an obvious advantage. Nanjing is rich in educational and scientific resources and has cultivated a large number of professionals. Meanwhile, emerging cities such as Nantong and Yangzhou are also developing vigorously. In such a highly competitive internal environment, there is still great potential for the development of integrated circuits in Suzhou.

Dr. Wang Xin further pointed out that by analyzing the layout of enterprises in the semiconductor industry chain within the park, It is evident that the semiconductor industry chain layout in the park is relatively complete, forming a system centered around 'design-Wafer manufacturing-Focused on 'encapsulation testing', supported by the equipment, raw materials and service industries, the park has a solid industrial foundation in chip design and packaging testing, and is one of the parks with a relatively complete industrial chain in China.

In addition, Dr. Wang Xin also stated that there are deficiencies in the development of Suzhou Industrial Park in the field of integrated circuit design, especially compared with strong integrated circuit industry parks such as Shanghai Lingang and Nanjing Jiangbei.

First, Against the backdrop of the major trend in digital economy development, Shanghai Lingang and Nanjing Jiangbei have successively deployed chip products in emerging fields. In comparison, the park can further expand its layout of core chip products in emerging application areas such as new energy and intelligent connected vehicles, industrial Internet, big data, and cloud computing.

Secondly, the integrated circuit design industry requires high-end talent, and the attractiveness of Suzhou Industrial Park to core R&D talents can be further enhanced. On one hand, the park's talent policy focuses on project support for major innovation teams and leading talents, and it needs to provide support for other core R&D personnel. On the other hand, the park urgently needs to improve its policy for high-skilled talents below master's degree level but in short supply in the integrated circuit design field to promote the development of the park's integrated circuit design industry.

Thirdly, Shanghai Lingang and Nanjing Jiangbei offer greater support for innovation links, and the support provided by the parks can be further enhanced.

Fourthly, comparing the layout of leading enterprises in industrial parks, Shanghai Lingang and Nanjing Jiangbei have larger-scale enterprises with comprehensive industrial chain coverage, while the scale of leading enterprises in the park can generally be expanded.

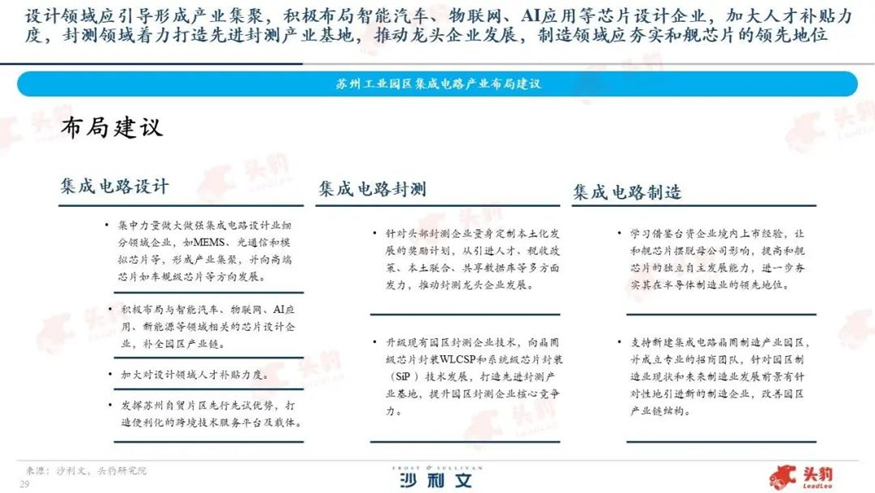

In response to the current development of integrated circuit industries in Suzhou Industrial Park, Dr. Wang Xin has put forward relevant layout suggestions.

First, Design industry It should guide the formation of industrial agglomerations and introduce technologies related to intelligent vehicles, Internet of Things,AIChip design companies related to applications and other fields should increase their efforts in introducing high-end talents for integrated circuit design, and leverage the advantages of Suzhou's free trade zone as a pilot area to create convenient cross-border technology service platforms and carriers; secondly, Closed beta industry Efforts should be made to build advanced foundry and testing industry bases, and promote the development of leading foundry and testing enterprises; finally, Manufacturing We should consolidate the leading position of Yinghe chips in the manufacturing industry, support the establishment of new wafer manufacturing industrial parks, and set up a professional investment promotion team to provide professional services to the team.

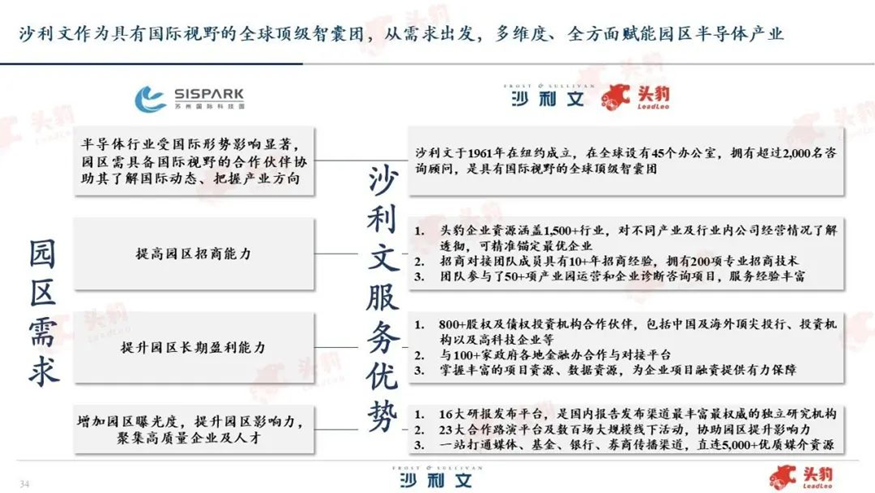

As a global top-tier think tank with an international perspective, Frost & Sullivan60Over the years, it has provided comprehensive services such as full life cycle investment and financing services, growth consulting services for a large number of enterprises at home and abroad. It has a deep understanding of market development laws and rich industrial ecological resources. LeadLeo is a leading original industry research content platform in China, serving as both an integrator of resources and an 'antenna and radar' for industry and corporate information. It provides timely and comprehensive understanding of enterprises and the industries they operate in. Frost & Sullivan and LeadLeo, starting from demand, can empower the semiconductor industry in the park in multiple dimensions and comprehensively.

Dr. Wang Xin expressed confidence that in the future, Frost & Sullivan and LeadLeo are very much looking forward to working with the park to understand industry trends, seize development opportunities, and jointly promote innovation and upgrading of China's semiconductor industry.