2023Annual Health Environment Electrical Appliance Industry Development Conference

11month24On the 1st, co-hosted by Huicong Water Purification Network and Huicong Air Purification and Fresh Air Network, the event “New Beginnings, Bold Actions ·Growth Against the Current→2023The Annual Health Environment Electrical Appliance Industry Development Conference was successfully held in Guangzhou.

The purpose of this conference is to focus on the latest ideas, technologies, and services in the world-leading health environment electrical appliance industry. With a holistic perspective and systematic layout, we aim to build an influential international event that sets up numerous sub-awards to discover brands and individuals who are shining in various fields such as product research and development, intelligent manufacturing, and model innovation. By collecting these 'highlights,' we intend to illuminate the glory of the industry. Starting from now, we explore new forces, trends, and futures in the health environment electrical appliance industry, using the power of examples to boost industry development.

Frost & SullivanFrost & SullivanChen Xialin, consulting manager of Frost & Sullivan's Greater China region, was invited to attend the event and delivered a speech on the theme of 'The Future Outlook of Commercial Water Purification'.

Consulting Manager, Greater China, Frost & Sullivan Chen Xialin

Chen Xialin stated that in the commercial sector, due to the outstanding advantages of water treated by water purifiers in various aspects, its market share is continuously increasing, gradually replacing bottled water and plain boiled water. The proportion of consumption of drinking water treated by water purifiers has changed from2018year12.5%Grew to2022year15.9%In recent years, commercial water purifiers have become very popular in scenarios such as office buildings, hospitals, enterprises, and government agencies. The water treated by water purifiers is gradually becoming the mainstream of commercial drinking water. It is estimated that by2027In 2024, its proportion will grow to25.8%.

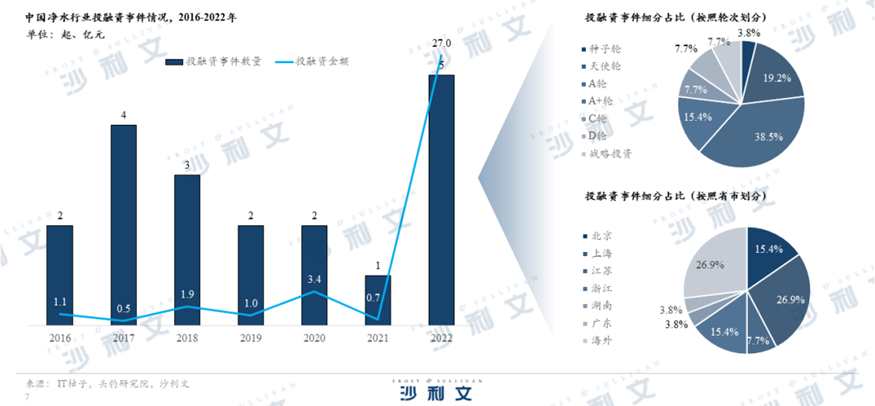

Judging from the investment and financing situation,2022In 2021, with economic recovery, strong downstream market demand, and increasing residents' attention to drinking water health, the number of investment and financing projects2021year1Rising sharply5At the beginning, the amount of investment and financing grew to27yuan, nearly7The highest year-on-year level was recorded, with an improvement in market prosperity. It is expected that in the future, as water purifiers become more widespread and their technology and services are updated and iterated, the popularity of the water purification industry will gradually rise.

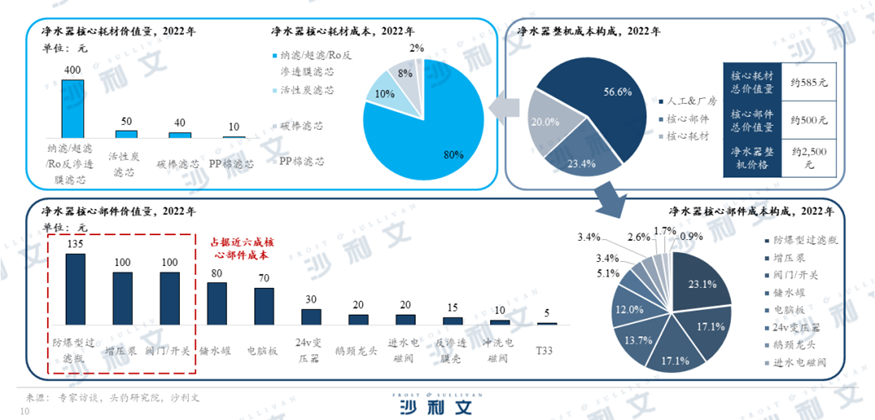

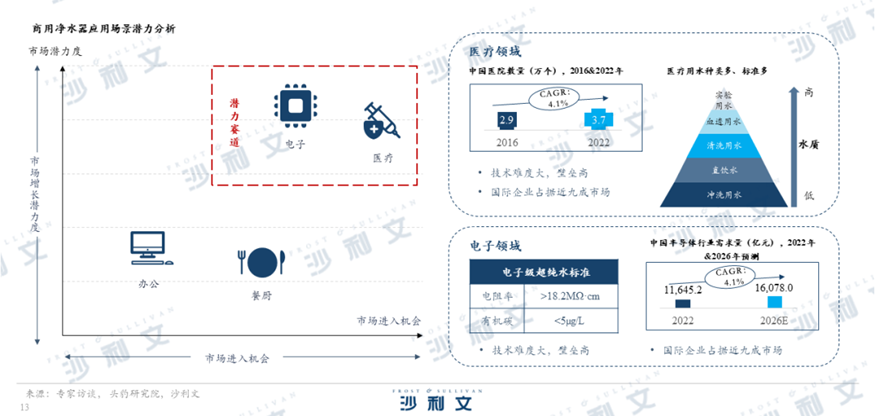

From the perspective of the industrial chain, the upstream of China's commercial water purifier industry consists of raw material suppliers, which are divided into core component suppliers and core consumables suppliers. Among them, core components account for a significant proportion of the total raw material costs.23.4%Proportion, with core consumables costs accounting for the entirety of raw material costs20.0%,45.8%For labor and factory costs. In the midstream of the industrial chain are water purifier manufacturers, divided into four categories: international brands, Chinese household appliance brands, Chinese water purification brands, and other brands. International brands have a high profile and market recognition, and possess technological advantages, occupying a high share in the market; Chinese brands have channel advantages, with well-known enterprises such as Midea and Haier also holding a certain market share. In the downstream of the industrial chain are the application scenarios for commercial water purifiers, with office use being the main scenario, accounting for a market share of60%The overall downstream coverage rate is at a low level, indicating significant potential for future development.

Chen Xialin pointed out that the total cost of a water purifier product can be divided into core component costs, core consumable costs, and labor and factory overhead costs, among which labor&The factory building occupies a relatively large proportion, accounting for56.6%This is mainly due to the improvement in manufacturers' service capabilities, which has led to increased labor costs. Consumables and components include four-stage filters, explosion-proof filter bottles, booster pumps, and valves./Switches have a high equivalent value.

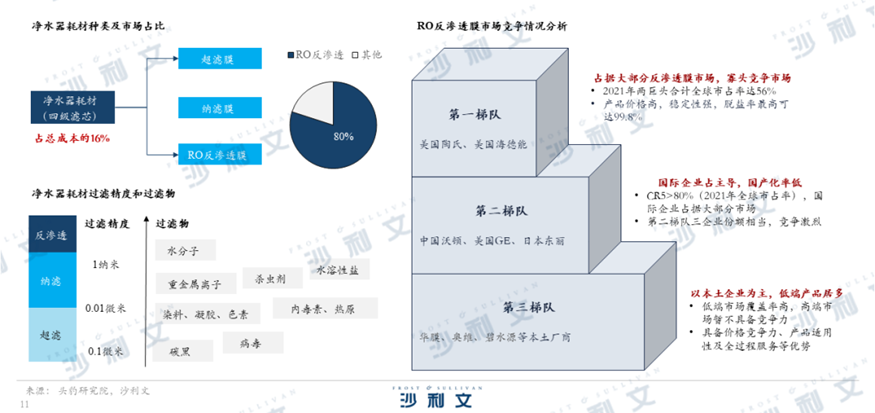

She further introduced that the fourth-stage filter element is key to the water purification process, and about 80% of products on the market use itROReverse osmosis membrane; currentlyROIn the reverse osmosis membrane market, international companies hold a dominant position. The first tier consists of Dow and Hydranautics from the United States, which account for more than half of the global reverse osmosis membrane market share, forming an oligopoly market. The second tier includes China's Wohlen and American companies.GEAnd Japan's Toray, in the marketTop 5Only one Chinese company,CR5>80%The localization rate is relatively low, with local enterprises covering the low-end market. However, they are promoting the localization process by leveraging price and applicability advantages.

Chen Xialin believes that among the four downstream application scenarios, the office scenario has a stable position for leading enterprises, making it difficult for new entrants to gain market share. The catering and kitchen scenario has a smaller market with relatively lower development potential; the electronic scenario and medical scenario have high technical difficulty, fewer participants, more market entry opportunities, and greater downstream demand, thus possessing more development potential.

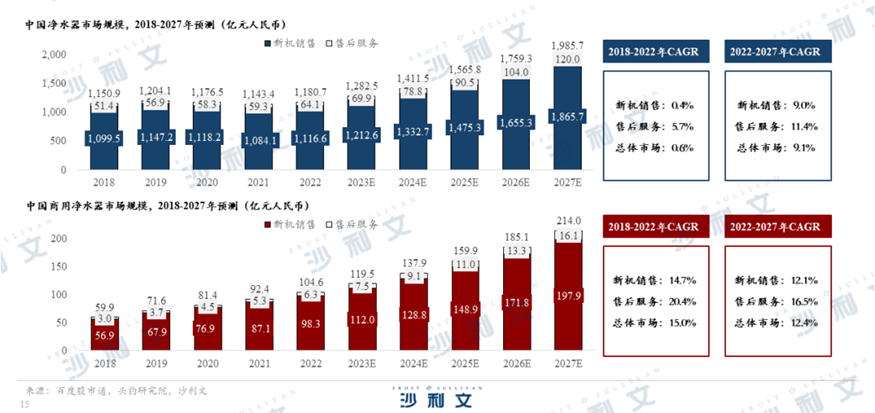

since2018Since [start year], the market scale of water purifiers in China has exceeded 100 billion yuan for several consecutive years. It is expected that the market will maintain rapid growth in the future.2027Annual achievement1,985.7Yuan. Commercial water purifiers are one of the fastest-growing categories in the water purifier market. With the increasing demand for commercial water purifiers in various downstream fields and the improvement of commercial water purifier ecosystem services, it is expected that by2027In [year], the market scale of commercial water purifiers in China will grow to214.0yuan,2022 - 2027yearCAGRreach12.4%The vast market scale has attracted more enterprises to deploy in the commercial water purifier sector.

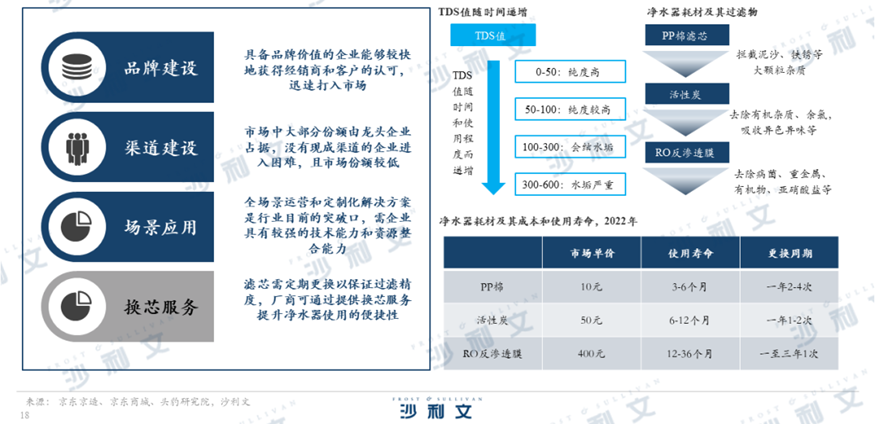

Chen Xialin stated that the core competitiveness of commercial water purifier companies mainly lies in brand building, channel development, and scenario applications. Brand value is crucial for a company to establish itself in the market; it is difficult for companies without established channels to enter the market; breakthroughs are needed in full-scenario operations and customization; moreover, manufacturers can alleviate the pain point of frequent filter replacements by improving service levels.

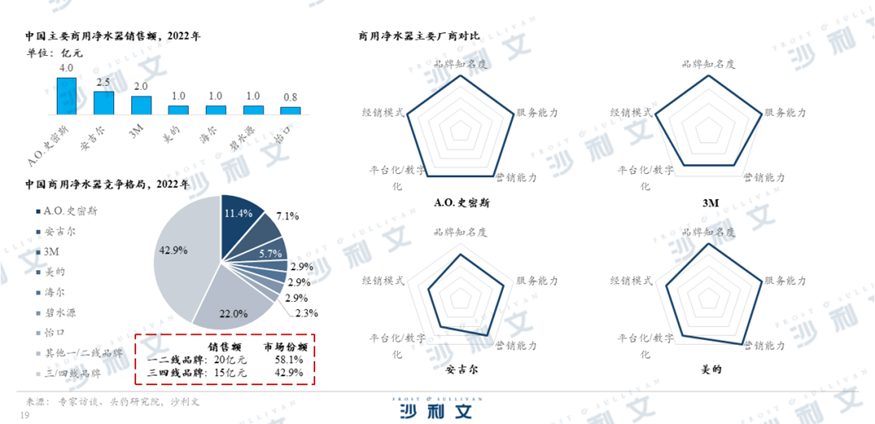

Subsequently, she pointed out that participants in the Chinese commercial water purifier market include international brands and domestic manufacturers. In terms of international brands,A.O.SmithA.O. Smith),3MWhile the company has established a certain market share and brand influence in the commercial water purifier market in China. These international brands have gained a certain market recognition after entering the Chinese market, leveraging their advantages in technology research and development, quality control, brand influence, etc. In terms of Chinese manufacturers, Angel (angelCompanies such as Midea and others hold a significant share in the commercial water purifier market. These Chinese enterprises have achieved certain success in research and development and production. By continuously innovating and improving product quality, they have gradually formed their own brand advantages and market position. Currently, there is not much gap between water purifier products from Chinese and international brands, and both can meet high water purification requirements. However, products from third- and fourth-tier brands may have stability issues compared to internationally renowned brands.

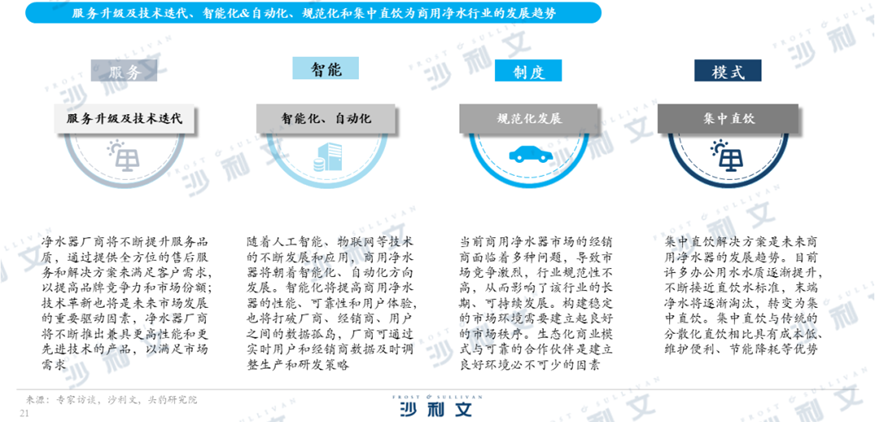

Finally, Chen Xialin concluded that the future development trend of the commercial water purifier market will mainly involve service upgrades, technological iterations, and intelligence.&Automation, standardization, and centralized direct drinking.

Water purifier manufacturers will continuously improve service quality and carry out technological innovation. By providing comprehensive after-sales service and solutions to meet customer needs, they will launch products with higher performance and more advanced technology to satisfy market demands, thereby enhancing brand competitiveness and market share.

The trend towards intelligence will improve the performance, reliability, and user experience of commercial water purifiers. It will also break down data silos among manufacturers, distributors, and users. Manufacturers can adjust production and R&D strategies in real time based on real-time user and distributor data.

Standardization means establishing a good market order for commercial water purifiers. An ecological business model and reliable partners are essential factors in creating a favorable environment.

Centralized direct drinking solutions are the future development trend for commercial water purifiers. Currently, the quality of office water is gradually improving, approaching the standards for direct drinking water. End-of-line water purification will gradually be phased out and replaced by centralized direct drinking. Compared with traditional decentralized direct drinking, centralized direct drinking has advantages such as lower costs, convenient maintenance, energy saving, and consumption reduction.