2024China Foodservice Industry Annual Conference

2024year2month26day-28On the day, initiated and hosted by the food industry, co-hosted by Ande ZhiLian, and co-organized by Huatang Yunshang, Food Industry Headlines, and Midea's Commercial Cold Chain Strategy, “2024The 'China Food Industry Leaders Annual Conference' was grandly held in Foshan. The annual China Food Industry Leaders Annual Conference is a premier event for the food industry at the beginning of the year, a high-end forum where food entrepreneurs gather, and also a predictive summit for the annual trend trends.

The 2024 China Food Industry Annual Conference is centered around the theme 'Finding an Ecological Niche', focusing on 'Economic Recovery and New Circulation', 'Cost-effective Food Trends', 'Category Franchising Growth', 'Consumer Differentiation', 'Promoting Agriculture to Food',AIFloor-to-ceiling food service scenarios", etc.30+The core topic guides the future direction and plans new strategies. Over the three-day period, the organizing committee also held several specialized forums such as the Overseas Expansion Forum and the Supply Chain Forum, providing a wealth of exchange and learning opportunities for the participants.

This annual conference has invited authoritative entrepreneur leaders, representatives of emerging brands, well-known economists, and industry chain service experts.300Industry leaders gathered together to conduct in-depth discussions on the theme of the annual conference. They jointly analyzed the development trends of industries, the core principles and future directions of enterprise development, offered strategies for industrial innovation and development, and sought solutions to navigate the economic maze towards a commercial future.

Frost & SullivanFrost & SullivanMr. Zhang Jian, Partner and Managing Director of Frost & Sullivan's Greater China Region, was invited to attend the event. With the theme of "Consumption: 'More and More Precise Spending'", he2024Zhang Jian stated that the improvement in upstream supply chain efficiency, along with more rational planning and astute choices by downstream consumers, has led to the coexistence of consumption upgrading and consumption degradation.

Partner and Managing Director of Frost & Sullivan Greater China Region Zhang Jian

Zhang Jian pointed out that from the perspective of macroeconomic conditions, China's economic development is undergoing a period of structural changes, evolving from a high-speed growth and dividend-generating phase to a phase of high-quality development and stable growth. Structural changes such as low fertility and population aging are putting pressure on economic development.

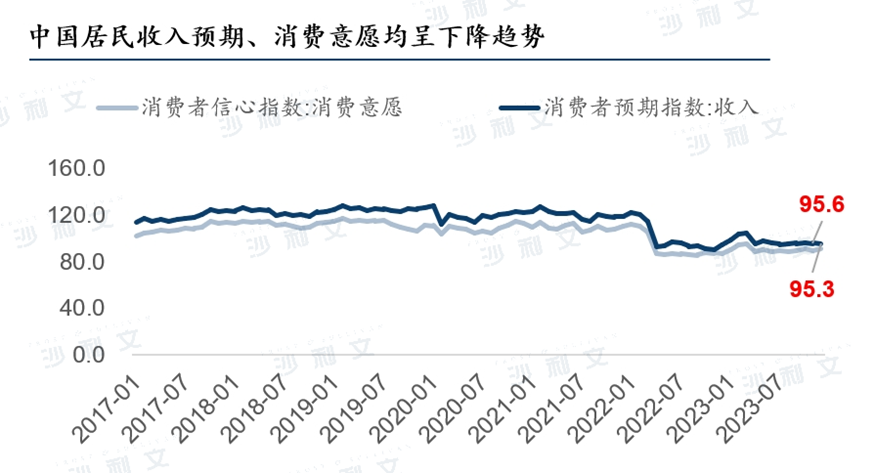

After the pandemic, the national economy has recovered in an orderly manner, and the prelude to a 'new cycle' has begun. Per capita consumption and disposable income among residents have gradually recovered from the severe blow of the pandemic.2023Per capita disposable income of residents across the country39,218Yuan, nominal growth compared with the previous year6.3%, after deducting price factors, actual growth6.1%, as compared to2022Real annual growth rate2.9%, there is an obvious improvement;2023In [year], per capita consumption expenditure of residents across the country was compared with2022Significant improvement was made in the year, for26,796Yuan, nominal growth compared with the previous year9.2%Actual growth after deducting the impact of price factors9.0%.

2022After the New Year, residents' expectations for future income and consumption intentions both declined. This was mainly due to various factors such as pessimistic sentiment caused by the pandemic, and deep adjustments in the real estate sector, which hit residents' confidence and willingness to consume. The pursuit of 'pragmatism' in product selection and lifestyle has become the main consumption trend among consumers after the pandemic.

Source: Analysis by Frost & Sullivan

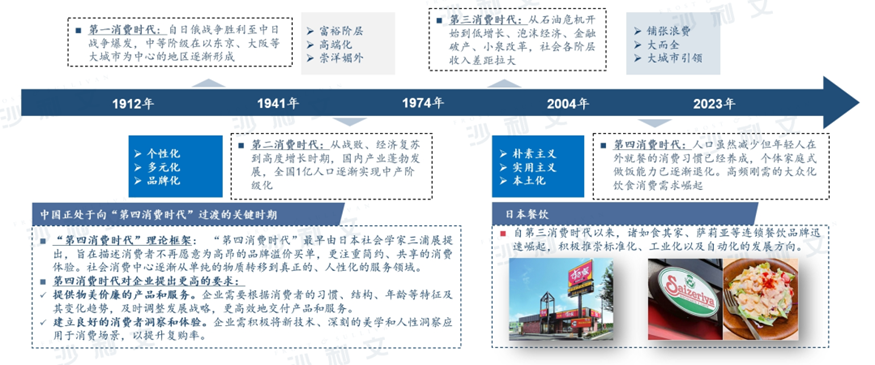

Despite the recent slowdown in economic development and the impact on consumer confidence, the Chinese economy still demonstrates strong resilience, which helps consumers build a cautious but optimistic sentiment. "The current Chinese consumer market has shown characteristics of the fourth consumption era, with consumption trends returning to simplicity and pragmatism. At the same time, the standardization, industrialization, and automation of the consumer industry continue to improve," said Zhang Jian.

Source: Analysis by Frost & Sullivan

From the perspective of consumer profiles, consumers' consumption concepts are gradually shifting towards pursuing high cost-effectiveness. The overall consumption level has decreased, conspicuous consumption has reduced, and the proportion of practical consumption has increased. Consumers are pursuing more rational planning and more astute choices. Consumption upgrades and downgrades coexist, with increased sensitivity to prices and a stronger trend towards rational consumption.

Speaking about the growth drivers of the consumer industry under the new situation, Zhang Jian said that the millennials,ZThe identified growth of segmented consumer groups across generations and the continued expansion of the middle class serve as growth engines for many consumer goods. In addition to population "deflation" and accelerating aging, born in1982 - 2009The 'millennium' of1995 - 2009Year's “ZGenerations" The proportion of the population that makes up the total population is about37%future20The average annual growth will be steady and rise, and in2060Around40%At the same time, China has the largest number of newly emerging middle-class families in the world. The continuous increase in upper-middle-income consumers will be the biggest driving force for China's consumption growth.

Meanwhile, the importance of Chinese brands in consumers' lives is increasing. In recent years, Chinese brands in multiple fields have gained the favor of consumers.2023year,79.9%Consumers of Chinese brands increased, exceeding2020year73.3%Consumers of all age groups have seen a significant increase in their consumption of Chinese brands.

With the enhancement of comprehensive national strength, Chinese brands are constantly pursuing innovation, focusing on quality upgrades, and strengthening the promotion of brand stories. 'Made in China' has shed its prejudice, not only being 'affordable', but also 'of high quality'. Chinese people are now willing to cast their 'trust' votes. The shift in consumer attitudes is driving the growth of local Chinese brands, with domestic enterprises winning the market. For the vast majority of consumers, Chinese brands have become their first choice in their hearts.

In addition, 'replacement products' are gradually becoming popular. Consumers are beginning to focus on cost-effectiveness, with 'products being the most fundamental hard power'. Considering consumers' real needs and creating high-quality products are new growth paths for the consumer industry.

Subsequently, Zhang Jianjian looked ahead to the new scenario application trends in the fields of catering, beverages, tourism, and digitization.

Zhang Jian stated that the catering industry generally can warm up faster during economic recovery periods and counteract the impact of economic downturns, demonstrating strong resilience and faster market recovery capabilities. It is one of the consumer industries with the most moat effect. China has become the world's second-largest catering market, with a catering scale second only to that of the United States. Compared to overseas countries, China's overall catering chain rate and market concentration are still at relatively low levels. In the future Leading enterprise There is great potential for development.

Source: Analysis by Frost & Sullivan

Data shows that the market scale of new tea drinks in China has changed from2017year422RMB billion growth to2022year1,040Yuan, with an annual compound growth rate of20%The penetration rate has increased rapidly,2022The penetration rate of the new year's tea drink target customer group exceeds40%New tea drinks2022The year is in the first half of the industry's mature development phase. Overall, the penetration rate of target customers exceeds 40%, both the number of stores and market scale growth have slowed down, the supply chain has begun to take shape, third- and fourth-tier cities have basically completed their layout, the market tends towards 'maturity', and there is still room for further penetration; looking at per capita store count and per capita caffeine intake, new tea drinks are still in the market formation stage.

Source: China Chain Operation Association2022'Trends in New Tea Drinks: A Report by Frost & Sullivan'

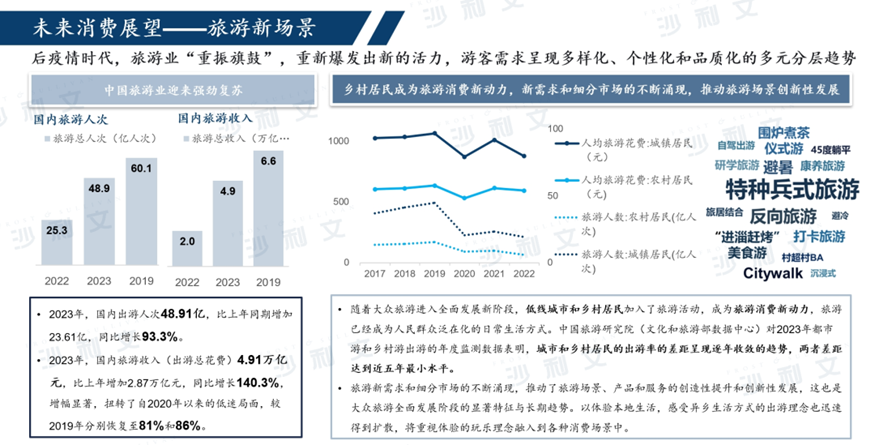

In the post-pandemic era, tourism has 'rejuvenated' and burst back with new vitality.2023Number of domestic outbound travel trips in48.91Yi, an increase compared with the same period last year23.611000 million, a year-on-year increase93.3%.2023Domestic tourism revenue (total travel expenditure)4.91trillion yuan, an increase compared with the previous year2.87trillion yuan, a year-on-year increase140.3%The growth rate has increased significantly, reversing the situation since2020The downturn since last year, compared2019Recovered to81%and86%Tourist demand shows a diversified, personalized, and quality-oriented multi-level trend, driving creative enhancement and innovative development of tourism scenarios, products, and services. This is also a significant characteristic and long-term trend in the comprehensive development stage of mass tourism.

Source: Ministry of Culture and Tourism, analysis by Frost & Sullivan

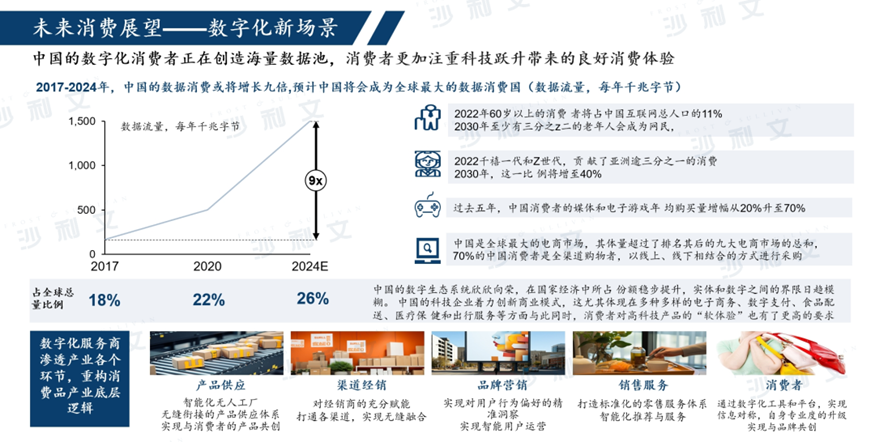

Chinese digital consumers are creating massive data pools, placing greater emphasis on the good consumer experience brought about by technological leaps. Digital service providers penetrate every link of the industry, reconstructing the underlying logic of the consumer goods industry. The intelligent unmanned factories in the product supply link seamlessly connect with consumers to co-create products; the fully empowered channel distribution link unblocks various channels, achieving seamless integration; the brand marketing link achieves precise insights into user behavior preferences, realizing intelligent user operations; the sales link creates a standardized retail service system, realizing intelligent recommendations and services; consumers, through digital tools and platforms, achieve information symmetry and upgrade their professionalism, realizing co-creation with brands.

Source: Analysis by Frost & Sullivan