"Innovation" has become the top keyword in the pharmaceutical industry in 2021. Looking at the approval of new drugs, this year at least 61 new drugs have been approved for marketing by the National Medical Products Administration (NMPA) of China, including 25 locally developed drugs. Both the overall number of approvals and the proportion of domestically innovative drugs have reached record highs. In terms of financing data, the COVID-19 pandemic has catalyzed a surge in healthcare capital, leading to a significant increase in financing events and amounts in 2021.

What stage is China's innovative drugs at? What problems in the R&D of innovative drugs in China need to be urgently addressed? How do multinational companies (MNCs) respond to China's innovation wave? For the future, is it "the future has come" or "the dividend has ended"?Zhu Yi, Executive Director of the Healthcare Business Unit in Greater China at Frost & Sullivan (referred to as 'Frost & Sullivan'), was interviewed by Blue Whale Finance. He discussed with you the development trends of the healthcare industry and the innovative drug market.

Blue Whale Finance

"Innovation" is undoubtedly the top keyword in the pharmaceutical industry in 2021.

In terms of new drug approvals, at least 61 new drugs have been approved for marketing by the National Medical Products Administration (NMPA) of China this year, including 25 locally developed drugs. Both the overall number of approvals and the proportion of domestically innovative drugs have reached record highs. In terms of financing data, domestically, the total financing for China's healthcare industry reached 100.234 billion yuan in the first half of 2021, a year-on-year increase of about 78.72%. The COVID-19 pandemic has catalyzed the influx of healthcare capital, leading to a significant increase in financing events and amounts in 2021.

However, alongside the rise of innovative drugs, there is also a problem of homogenization of innovative targets. In 2020, the Drug Clinical Trial Registration and Information Publicity Platform registered a total of 2,602 clinical trials. However, among the top 10 target varieties registered for clinical trials, the total number of varieties reached as many as 389, accounting for over 10%, indicating severe competition.

In the face of the vigorous development of innovative drugs in China, how are multinational pharmaceutical companies (MNCs) headquartered in China actively responding? It is evident that they are increasingly willing to invest resources in China's innovation sector, whether it be in clinical BD, incubation, or investment.

In 2021, what stage is China's innovative drugs at? What problems in the R&D of innovative drugs in China need to be addressed urgently? How do multinational companies (MNCs) respond to China's innovation wave? For the future, is it 'the future has come' or 'the dividend has ended'?

With favorable policies, the approval rate of domestic innovative drugs reached a new high in 2021.

Since the reform of drug review in 2015, the policy side has continuously released positive signals to promote the adjustment of the domestic pharmaceutical industry structure and technological innovation. With the deepening reform of the drug approval system, a series of policy combinations such as the pilot program for drug marketing authorization holders, quality and efficacy consistency evaluation of generic drugs, and dynamic adjustment mechanisms of medical insurance catalogs have been introduced. These have completely changed issues such as insufficient R&D resources, slow review progress, low bidding efficiency, high hospitalization difficulty, and difficulties in connecting with medical insurance in the traditional pharmaceutical industry. They have greatly accelerated the rapid market launch of innovative drugs in China, promoted centralized procurement of drugs, and medical insurance payment processes. This has completely overturned the original R&D and sales model dominated by generic drugs in the Chinese pharmaceutical industry, and since then, the era of pharmaceutical innovation in China has developed vigorously.

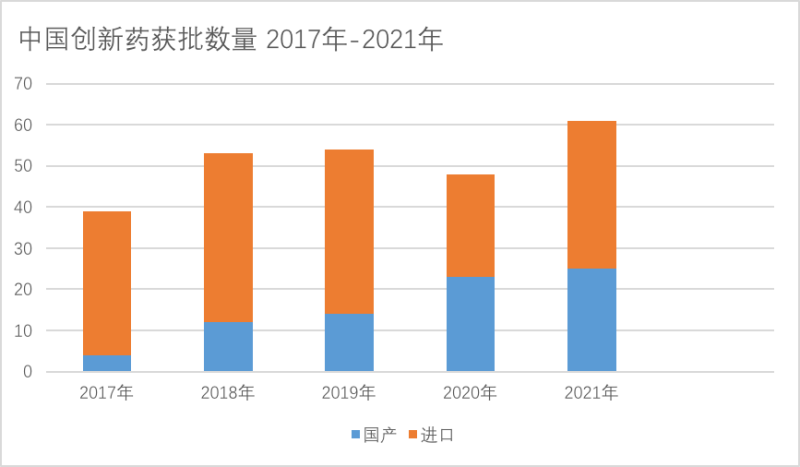

From the perspective of approval status, according to incomplete statistics by Blue Whale Finance reporters, since 2021 (December 29), at least 61 new drugs have been approved for marketing by the National Medical Products Administration (NMPA) of China. Among them, there are 25 domestically produced and 36 imported new drugs. Compared with previous years, both in terms of overall approval status and the proportion of domestically innovative drugs, this year has set a new historical high. In comparison, in 2017, a total of 39 new drugs were approved, including 4 domestically produced and 36 imported ones; in 2018, there were a total of 53 new drugs approved, including 12 domestically produced and 41 imported ones; in 2019, there were a total of 54 new drugs approved, including 14 domestically produced and 40 imported ones; in 2020, there were a total of 48 new drugs approved, including 23 domestically produced and 25 imported ones. It can be seen that in 2017, the number of imported innovative drugs approved was significantly higher than that of domestic innovative drugs. However, today, due to various forms such as independent research and development and authorized introduction by local enterprises, the R&D progress is gradually aligning with international standards.

Data source: Compiled by Blue Whale Finance reporter

This year, the breakthroughs in some cutting-edge technologies have attracted strong industry attention upon approval for market launch. For instance, two CAR-T therapies approved domestically this year, from Fosun Kite and WuXi AppTec, respectively, are novel tumor immunotherapy methods that can be precise, rapid, efficient, and potentially cure cancer. The attention paid to these not only lies in their anticipated therapeutic efficacy but also in their often-millions-dollar treatment costs. How to commercialize these is a topic that high-value innovative therapies face next.

In addition, the COVID-19 pandemic continues, and drug breakthroughs remain a hot topic of concern. On December 8th, the National Medical Products Administration (NMPA) of China announced that it had emergency approved the registration applications for the combination therapy drugs Anbalimab Injection (BRII-196) and Remdesivir Monotherapy Injection (BRII-198), which are subsidiaries of Tengsheng Bio-Tech Group Co., Ltd. The country has finally welcomed its first independently developed neutralizing antibody combination therapy, achieving a zero breakthrough. In terms of funding, according to the prediction of Industrial Securities, the commercial market space for neutralizing antibody drugs for treating COVID-19 can reach $6.9 billion to $14.6 billion (RMB 44.8 billion to RMB 94.9 billion), indicating broad profit margins for neutralizing antibodies. Whether in terms of social attention or capital preference, the development of COVID-19 drugs undoubtedly touches the nerves of the public and capital.

In China, multiple COVID-19 drugs are racing against each other. The neutralizing antibody therapy DXP604, jointly developed by the team of Xie Xiaoliang from Peking University and Danxu Biotech, is undergoing phase II clinical trials in China; Junshi Biosciences has three COVID-19 treatment drugs advancing, including two neutralizing antibody therapies and one oral medication; in terms of oral medications, Azvudine, developed by Henan Normal University, is currently conducting phase III clinical trials in China, Brazil, and Russia, aiming to apply for conditional approval for marketing in December; Pekluramide, a promising drug developer, is conducting international multi-center phase III clinical trials in China, the United States, and Brazil, and has already obtained an Emergency Use Authorization (EUA) in Uruguay.

China and global healthcare financing reach new highs, with innovation in China moving closer to First-in-Class status

According to the statistical analysis by Deng Yunting, an analyst at LeadLeo Research Institute, with the changes in the pandemic, the healthcare sector has seen broad application prospects, high risk resistance capabilities, and is more favored by capital markets. In 2020, global healthcare financing reached a record high, a year-on-year increase of 53%. In the second quarter of 2021, global financing amounted to as high as $31.224 billion, a year-on-year increase of 68.10%.

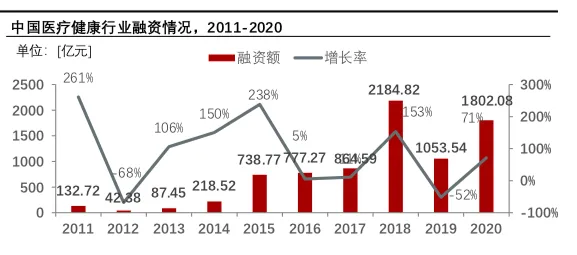

According to data compiled by the 'LeadLeo' research institute, in China, the total financing for the healthcare industry reached 100.234 billion yuan in the first half of 2021, a year-on-year increase of about 78.72%. In 2020, the total investment and financing for the healthcare industry reached 180.208 billion yuan, a year-on-year increase of 71%. Due to the short-term tightening of funds caused by the COVID-19 pandemic in the first half of 2020, financing projects for the healthcare industry dropped significantly. With the improvement in pandemic control, funds surged into the healthcare industry in the second half of the year, resulting in 470 financing events and raising over 100 billion yuan, bringing the total financing for 2020 to as high as 180.208 billion yuan.

Data source: LeadLeo Research Institute

Deng Yunting stated that biopharmaceuticals, internet healthcare, medical informatization, and the IVD field are hot investment and financing topics in global healthcare. In terms of biomedicine, cell and gene therapy, PROTAC, and ADC drugs have become hotspots. Following small molecule and antibody drugs, cell and gene therapy is expected to lead the next wave of treatment technologies. With products such as CAR-T being approved in China one after another, the market size for cell and gene therapy (CGT) in China is expected to reach $2.59 billion by 2025, with a CAGR (compound annual growth rate) of up to 276% from 2020 to 2025. The protein degradation targeting conjugate (PROTAC) track is poised to emerge, with Sequoia, Honghui, Tonghe Yucheng, and others investing early in related innovative pharmaceutical companies, and many Chinese pharmaceutical companies have also made arrangements. The global ADC drug market is rapidly expanding, with a significant acceleration in product launch speed in the past two years. China's ADC research pipeline is also poised to emerge, including the independently developed vedotinib by Rongchang Biotech, which was approved in June 2021, and the Chinese ADC market is about to enter a golden period.

Regarding the question of what stage China's innovative drugs are in, Zhang Xiao, a partner at Yikai Capital and head of the pharmaceutical and biotechnology group, stated that China's R&D of innovative drugs started with generic drugs, went through the Me-too and Me-better phases, and is currently in a transitional period towards Best-in-Class, while also standing at a critical juncture for transitioning to First-in-Class.

"When Chinese innovative drugs first started, although domestic companies had accumulated some experience in small molecule generic drugs, they still lagged far behind overseas in terms of talent, technology, and regulatory policies. The capital market was also not fully developed, and innovation mainly focused on the research and development of Me-too drugs, which could be 10 years or more behind original research drugs. From 2010 to 2015, Chinese innovative drugs entered a transformation period, with overseas talents returning to China with R&D experience to join the wave of innovation. The time gap between Fast-Follow drugs and original research drugs was shortened to within 5 years, and molecules with the potential for Best-in-Class emerged. After 2015, the Chinese innovative drug market flourished, with review and approval gradually aligning with international standards. Chinese innovative drugs began to enter overseas markets, several products reached cooperation agreements with major international pharmaceutical companies, and capital reached an unprecedented level," said Zhang Xiao.

Zhang Xiao stated: Currently, China's innovative drugs are still in the transition period to Best-in-Class status. However, it should be noted that the differentiated R&D of drugs targeting the same target has high technical barriers. True B-I-C (Breakthrough-Into-Class) innovation should ultimately reflect differences sufficient to alter medication choices during actual clinical treatment applications. Taking PD-1 as an example, the current market competition is more about commercial layout. In terms of B-I-C drug innovation, Chinese innovative drugs still face challenges but also have tremendous opportunities.

Target homogenization is evident, and a lack of source innovation is caused by multiple factors

The breakthrough of innovative drugs in China must overcome the homogenization of innovation targets. On November 10th, the Center for Drug Evaluation of the National Medical Products Administration released the 'Annual Report on the Current Status of Clinical Trials for New Drug Registration in China (2020)', which is the first report to comprehensively summarize and analyze the current status of clinical trials for new drug registration in China.

The Report points out that the number of new drug clinical trials and the variety of drugs in China have increased significantly compared to previous years. At the same time, Class 1 new drugs account for a relatively high proportion. However, the distribution of drug targets and indications is relatively concentrated, indicating that while new drug clinical trials are developing rapidly in China, there is also a problem of homogenization in clinical trials.

The report shows that in 2020, the Drug Clinical Trial Registration and Information Publicity Platform registered a total of 2602 clinical trials. However, the top 10 target drugs registered for clinical trials were PD-1, CYP51A1, VEGFR, PD-L1, DNA, EGFR, microtubule, HER2, GLP-1R, and JAK1, with a total number of 389 varieties, accounting for more than 10%.

In terms of the number of clinical trials, the aforementioned top 10 targets also have a highly concentrated clinical presence. Among them, more than 60 clinical trials have been conducted for targets such as PD-1, VEGFR, and PD-L1, with nearly 100 clinical trials targeting the PD-1 target alone.

Additionally, in terms of indications, clinical trials are mainly concentrated in areas such as anti-tumor and anti-infection. The indications for biologics and chemical drugs are primarily anti-tumor, accounting for 42.1% and 47.3%, respectively.

Zhu Yi, Executive Director of the Healthcare Business Unit at Frost & Sullivan Greater China, pointed out that although China has a rich pipeline of innovative drugs, there is serious homogenization. Taking PD-1/L1 inhibitors as an example, as of December 28, 2021, the Chinese NMPA had approved 11 products, including up to seven domestically produced innovative varieties, which is the highest number in the world. Similar phenomena are also occurring in the research and development of other popular targets. Homogeneous competition has led to waste of innovative R&D resources and indirect encroachment on the R&D resources for other clinical needs. Therefore, how to guide the rational allocation of innovative R&D resources will be an important matter for China's innovative development.

Regarding the issue of innovation homogenization, Zhang Xiao interprets the concentration on the research and development of popular targets as a lack of source innovation. He points out that the current lack of source innovation is the result of multiple dimensions influencing it. Firstly, there is still a gap between China's scientific research and translational levels compared to overseas, with the university research evaluation system being biased towards projects with lower risks and clear outputs. The average conversion rate of effective patents into products for industries is less than 10%.

Secondly, payment-side bottlenecks limit the flow of capital towards source innovation. In the United States, small enterprises lead innovation, with multinational pharmaceutical companies supporting them through incubation or product introduction while taking on R&D risks. MNCs add and terminate pipelines at a similar rate each year, making high R&D risk a norm. Currently, the cooperation of leading large pharmaceutical companies in China mainly focuses on mature products, increasing the pressure on biotech companies to invest in clinical manpower and funds.

Finally, at the capital end, the proportion of venture capital funds used in China to support incubation and transformation is much lower than that of leading global biopharmaceutical countries. At the same time, the capital market's ability to absorb clinical failures is still relatively low, with the primary and secondary markets essentially tending towards risk aversion, resulting in certain financial pressure on source innovation.

The changes of giants under China's innovation

Driven by innovation in China, for multinational pharmaceutical companies (MNCs), the Chinese market and innovation are becoming increasingly important. It can be seen that they are increasingly willing to invest resources in China's innovation, whether it is in clinical BD, incubation, investment, or other aspects.

In terms of clinical practice, China has gradually become part of the global clinical trials conducted by multinational corporations (MNCs). Novartis announced an adjustment to its R&D strategy in China, planning to make Shanghai's R&D center a global excellence center for early clinical development of drugs on Novartis' R&D pipeline. Boehringer Ingelheim launched the China In and China Key projects, defaulting to include all Boehringer Ingelheim's early clinical and global registration studies in China, enabling China to submit drug marketing applications simultaneously with the United States, the European Union, and Japan.

In terms of product BD, taking Amgen's strategic cooperation with BeiGene on multiple products as an example, in 2020, MNC accelerated its cooperation with Chinese pharmaceutical companies both through license-in and license-out. Numerous collaborations such as Roche's license-out deal for the development of a universal CAR-T and TCB bispecific antibody with Innovent Biologics, as well as AbbVie's license-in deal for the introduction of the Tianjing CD47 monoclonal antibody, reflect MNC's recognition of the R&D and execution capabilities of Chinese pharmaceutical companies.

In terms of incubation, more and more multinational corporations (MNCs) are starting to establish innovation incubators in China, deeply participating in Chinese innovation. Roche's accelerator located in Zhangjiang, Shanghai is the first accelerator independently established and operated by Roche globally. Startups that join can receive full-chain resource support from Roche, ranging from early research and development to later commercialization, as well as opportunities for financial support such as research funds. Similar incubators include Merck Innovation Center and Johnson & Johnson's JLABS incubator.

In terms of investment, MNCs participate in the Chinese innovative drug market through direct investment or by investing in funds. The Global Healthcare Industry Fund jointly established by AstraZeneca and CICC Capital is AstraZeneca's first healthcare industry fund raised globally and has so far been the largest in scale. Sanofi has made strategic investments in Kite Pharma Innovation Fund, indirectly supporting Chinese healthcare startups.

The future is promising

Regarding the prospects for where future innovative drugs will go, Zhang Xiao stated that resource influx, crowded competition tracks, full-fledged competition, and rational capital returns are inevitable stages for every emerging industry. Continuous experimentation and trial-and-error are also signs that the research and development of innovative drugs remains active.

He stated that the integration of technologies such as AI with pharmaceuticals in the future is expected to bring new technical means for target discovery and drug development, helping to improve R&D efficiency and success rates. The continuous development of industries such as CXO can also contribute to optimizing resource allocation. There are still vast blue oceans waiting to be explored in specialized tracks like ophthalmology. In very specific areas, there is a smaller gap between Chinese innovative drugs and world-leading levels, and overseas R&D stages are still early, potentially offering opportunities for overtaking on a curve. For example, gene editing, mRNA, and iPSC are fields that have seen many outstanding scientists participating recently, with high capital support and investment.

"Although there is still a long way to go for China's innovative drugs to reach a complete and mature ecosystem, it also harbors countless opportunities, and the future is promising," said Zhang Xiao.

*This article is reprinted from 'Blue Whale Finance', authored by Tu Jun, with the original title 'Review and Outlook | The difficulty of listing as an innovation highlight masks the embarrassment of insufficient source innovation. Is local innovative drug 'the future has come' or 'dividend has ended'?'.