With the relaxation of the three-child policy, the industry chain related to the three-child policy has developed rapidly, bringing new development opportunities to maternity centers. Maternity centers have attracted more and more young customers with their high-quality professional services, comfortable and calm environment, and provision of parenting knowledge and health education. Driven by market demand, the Chinese maternity center industry has developed rapidly. However, due to low entry barriers and uneven quality in the market, maternity centers are facing challenges such as reputation differentiation and regulation.

On July 9th, CCTV's 'Point Finance' program conducted a survey and report on the current state of the Chinese maternity center market, inviting Zhu Yiming, Senior Consulting Director at Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan'), to interpret the current market development status and future trends of Chinese maternity centers.

Zhu Yiming stated thatcompared to mature markets like Taiwan, the Chinese mainland market has a relatively lower penetration rate due to its late start, with a market penetration rate of less than 10%. The main reason is the high cost, which discourages many Chinese women from choosing it as a place for postpartum recovery.

‘The maternity center industry is a high-investment, high-return industry. The amount of initial capital depends on factors such as premises, operational models, facility procurement, and personnel. Most maternity centers target the mid-to-high-end consumer group, attracting customers through a professional image, so they usually incur significant expenses on luxurious interior decoration and professional staff training. To quickly get funds back, maternity centers often bundle different services and products and require customers to pay full fees in advance.’ he said.

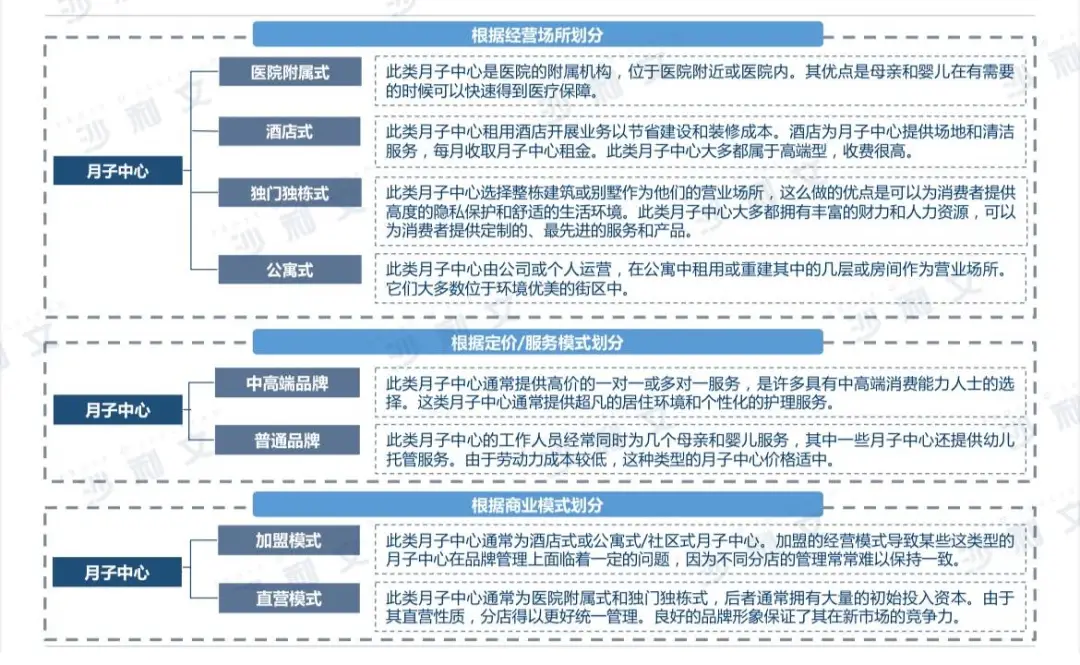

Classification of the Chinese maternity center industry

Source: Frost & Sullivan

On the other hand, the midwife industry in China has a long history and solid foundation. Therefore, most people (especially the middle and lower classes) still choose midwives to provide postpartum care.

In terms of distribution areas, maternity centers are currently mainly concentrated in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, and are gradually expanding to second- and third-tier cities.However, due to incomplete policy guidance and the high profit returns of the industry, many small enterprises have also joined the market, leading to low market concentration and service quality differentiation.

Source: Frost & Sullivan

‘We currently observe that the entire market is relatively fragmented. The main reason for this fragmentation is the presence of a large number of small workshop-style institutions and a few branded chains, which differ greatly in standard operations, service quality, specialized teams, and user experience.’ Zhu Yiming said. In addition, Chinese maternity centers also face competition from professional hospitals, making overall industry competition very fierce.

As the number of market participants continues to increase, competition in this market will further intensify. Zhu Yiming believes that companies under pressure from peer competition will have to change their management models.In the future,the management model of maternity centers will shift from extensive to refined, accelerating market reshuffling. Some maternity centers with flexible management and high operational efficiency will stand out in market competition, affecting a regionally expanded scope to the whole country.At the same time, the market price system will tend to become standardized, achieving hierarchical development.

‘Currently, the competitive differences in maternity centers mainly focus on hardware resources, such as the overall environment and supporting facilities. However, the homogenization of hardware resources will inevitably make price competition in maternity centers even more intense.Therefore, through innovation to diversify services and seek differentiated positioning will become an inevitable trend in the market.‘He emphasized.’

Frost & Sullivan has long been concerned about the development of the maternal and infant track, having a profound understanding and in-depth research on the industry. According to Frost & Sullivan data, from 2016 to 2018, the market consumer population in China's maternal and infant health management industry increased from 2.745 million people per year to 2.92 million people per year. However, the entire maternal and infant health management market is still in a highly unsaturated state. For example, in 2018, the market consumer population was less than one-fourth of the potential market demand population.

Overall, the market space for China's maternal and infant health management industry is still huge, especially for institutional services such as maternity centers and physical examination centers. From 2019 to 2025, it is expected that the number of market consumers will steadily rise, from 2.992 million people per year to 3.300 million people per year.In terms of demand saturation, although the market consumer population has improved to some extent, the entire maternal and infant health management industry is still a blue ocean.

*The video for this article is provided by CCTV's 'Point Finance' program.