10month21day2022Power Health Fund 5th EditionCEOThe forum and pharmaceutical investor conference was held in Shanghai, with the theme of 'Good Planning, Good Execution'. Frost & SullivanFrost & SullivanDr. Wang Xin, Global Partner and President of Greater China at Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan'), was invited to attend the conference and delivered an opening speech for the 'Impact Report' session, with the theme 'New Investment in Biotechnology'.

Global Partner and President, Greater China at Frost & Sullivan Dr. Wang Xin

At the beginning of his speech, Dr. Wang Xin analyzed the development opportunities in China's healthcare market. According to him, China has become the world's second-largest pharmaceutical market, but per capita medical expenditure is less than one-tenth that of the United States, indicating that there is still tremendous growth potential in China's pharmaceutical market.

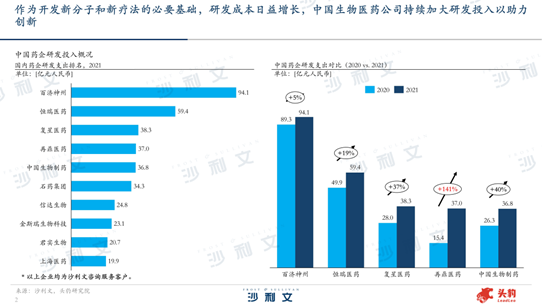

Dr. Wang Xin pointed out that as a necessary foundation for developing new molecules and new therapies, the R&D costs of enterprises are increasing day by day. Chinese biopharmaceutical companies continue to increase their R&D investment to support innovation, especially in the pharmaceutical industry2021It is also not difficult to see from the R&D investment ranking of the year that capital is crucial for the development of biotech companies.

Although affected by the COVID-19 pandemic, cross-border mergers and acquisitions have decreased significantly in recent years, biotech companies are actively introducing advanced R&D technologies from home and abroad.License-in grantedTransactions continue to set new highs in terms of volume and value, involving multiple emerging medical fields. According to statistics,2021In [year], Chinese pharmaceutical companiesLicense-in AcquisitionThe number of transactions has reached130Yuqi, with most transaction volumes exceeding1billion US dollars, with some transactions exceeding3billions, product selection involves dual antibodies,siRNA,mRNAVaccines, cell therapy,ADCand many other emerging fields.

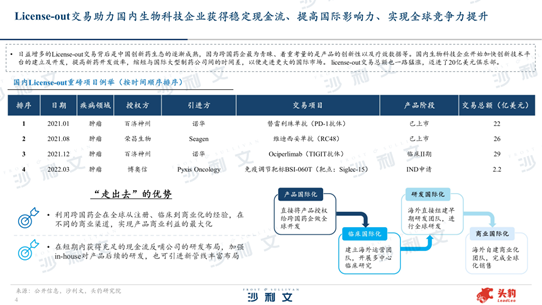

Meanwhile, biotech companies are also constantlyLicense-out of the MainlandTransactions bring domestic technology abroad to generate stable cash flows, enhance international influence, and facilitate better participation in global competition through cooperation with multinational enterprises. Currently, the steps for biotech companies to innovate and go global can be divided into4Stage one: The first step is product internationalization, directly authorizing the product to multinational pharmaceutical companies for global development; the second step is clinical internationalization, establishing overseas operational teams and conducting multi-center clinical research; the third step is R&D internationalization, directly forming early R&D teams overseas for global R&D; the fourth step is commercial internationalization, building a commercial team overseas to complete globalization sales. "Today, Chinese enterprises have completed the first two steps of product and clinical internationalization, and some have even started setting up R&D departments abroad. China's innovation drug R&D capabilities and its ability to export products overseas are expected to further improve," said Dr. Wang Xin.

Overall, the level of domestic innovative drugs has been continuously improving under policy incentives. The R&D level of innovative drugs is growing day by day, and the development of COVID-19 vaccines has also driven rapid technological development in the industry. It is believed that under the guidance of national policies, nurturing from the global market, and catalysis by the COVID-19 pandemic,2022In 2021, China's healthcare industry will increasingly integrate into the global innovation pulse.

Subsequently, Dr. Wang Xin analyzed the performance of the healthcare industry in the capital market for the guests present.

Dr. Wang Xin first introduced Compiled especially for cloud technology The 'Frost & Sullivan Frost & Sullivan index series', which consists of two indices, namely: Frost & Sullivan's Select Biotechnology Index30The Composite Index of Biotechnology, which includes both the Hang Seng Biotech Index and the Frost & Sullivan Index. Both indices have their own characteristics, focusing on different needs of all parties in the market and highlighting the Hong Kong Stock Exchange from their respective perspectives.18AGroup characteristics of the biotechnology sector and listed companies.

Frost & Sullivan featured30index by30The Hong Kong Stock Exchange, which has the greatest market influence and strongest representativeness18AThe constituent index of biotech listed companies is positioned to accurately reflect18AThe overall performance of the most representative companies in the sector. The index undergoes regular sample adjustments quarterly to ensure the representativeness and timeliness of the index's constituent stocks. The index adopts a free float market value weighting method and has a weight cap for its constituent stocks to ensure the high investability of the index, as well as to depict the Hong Kong Stock Exchange from the perspective of investors.18ARational investment expectations in the biotechnology sector.

Frost & Sullivan's Comprehensive Index of Biotechnology Companies from all18AThe constituent index of Biotech Listed Companies includes companies that follow the Hong Kong Stock Exchange.18AWhen a company goes public, the index will include its shares in the index sample before the market opens on the first day of listing to ensure that the index fully represents the sector. The Bio-Comprehensive Index specifically adopts the total market value weighting method to reflect the overall issuance structure characteristic of biotech companies with less publicly offered shares at their initial listing, restore the true influence of enterprises, and depict the overall investment and financing heat of the sector.

In addition, cloud technology has also compiled supplementary indicators for the Frost & Sullivan Greater China Biotechnology Index series based on statistical data, to complement the index series and assist all market participants in comprehensively understanding the Hong Kong-listed18AThe rules implement other overall operational characteristics of listed biotech companies.

"The 'Frost & Sullivan index series' reflects Hong Kong stocks."18AWe hope that the overall operating characteristics of stock prices of listed companies in the biotechnology industry can help market participants such as investors, listed companies, and capital market intermediaries to understand comprehensively and deeply.18AThe biotechnology sector provides reference tools for sector investment research.” said Dr. Wang Xin.

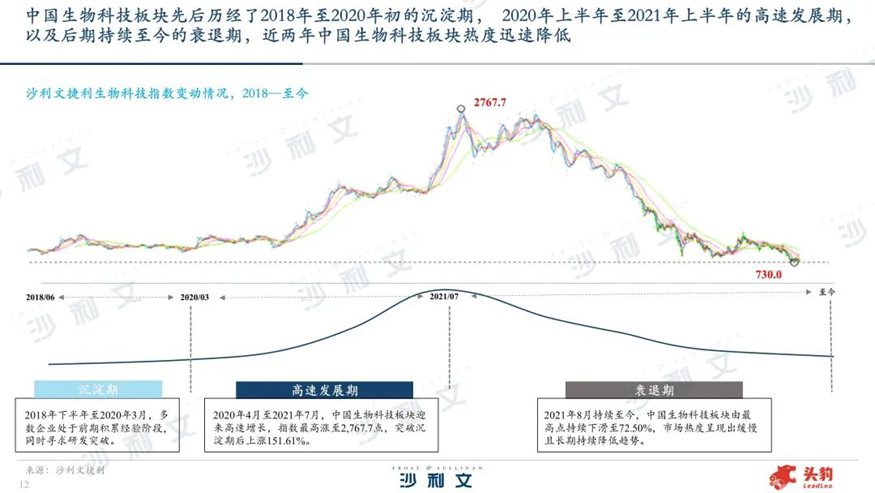

According to the changes in the Frost & Sullivan Jili Biotechnology Index, China's biotechnology sector has gone through2018Year to2020The initial settling period,2020First half of the year to2021During the high-speed development period in the first half of the year and the subsequent recession that has continued to this day, the interest in China's biotechnology sector has rapidly declined in the past two years.

2022In the first half of the year, there were certain fluctuations in global and Chinese capital markets. From a global perspective, financing rounds for the global healthcare industry gradually shifted back to earlier stages, with early-stage investment companies gradually growing stronger. At the same time, exceeding1The proportion of large financing events worth hundreds of millions has increased, and the scale effect of enterprises is gradually emerging. It can be seen that investment institutions tend to choose high-quality targets with clearer business models and higher stability. Unlike globally,2021In China in1The proportion of large-value financing events in hundreds of millions of dollars has decreased rather than increased. In the future, the rounds of financing for China's healthcare sector will gradually move backward, indicating that capital investment is more cautious, investments are becoming rational, and there is a preference for mature targets.

In the post-pandemic era, the healthcare sector has gradually gained more attention due to public interest. Major medical enterprises have seen significant performance growth, and their potential and growth prospects have been further explored. In the future, this is expected to accelerate capital entry.

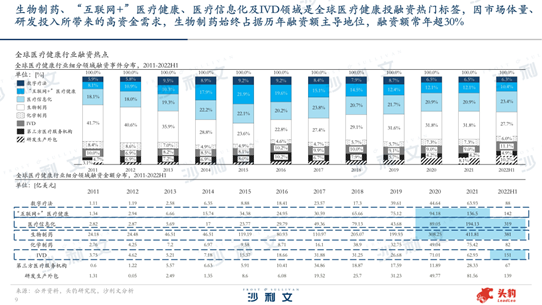

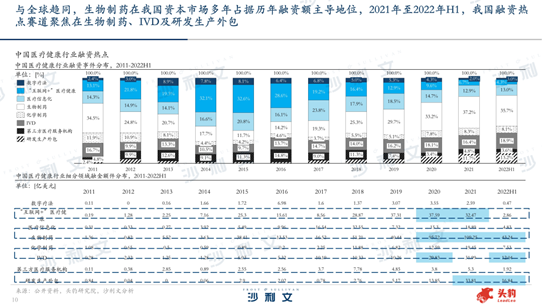

Biopharmaceuticals, “Internet+"Medical health, medical informatization, andIVDThe domain is a popular tag for global healthcare investment and financing.

Among them, due to the high capital demand brought about by market size and R&D investment, biopharmaceuticals have always dominated the financing amount over the years, with the financing amount exceeding30%.2021In the year, the global biopharmaceutical field totaled880Start trading, with411.81The financing amount of hundreds of millions of US dollars ranks first in the healthcare sub-sector, while in the field of medical informatization550Start trading,194.13USD 10 billion followed, “Internet+"Medical health andIVDRanked third and fourth in the field.

Compared with2021For the first half of the year,2022In the first half of the year, global total financing and the number of financing events in various sectors all declined to varying degrees.2022In the first half of the year, there were a total of568Financing events, a year-on-year decrease163rise; total financing reached nearly200billion US dollars (about RMB1,300(Yi-billion), a year-on-year decrease of about37%.

In line with global convergence, biopharmaceuticals have long held a dominant position in the healthcare segment of China's capital market. In addition,IVDR&D and production outsourcingCDMOAlso highly favored by the capital market.

forIVDOn the one hand, this is due to a significant increase in performance in epidemic-related sectors such as in vitro diagnostics. On the other hand, there are various factors such as the implementation of volume-based procurement for medical devices, lower listing thresholds, relatively lower risks and higher certainty compared to innovative drugs, and greater space for domestic substitution, which have made the medical device sector once again an important target for capital allocation.

Regarding R&D and production outsourcing, on the one hand, China's pharmaceutical industry is in an industry stage transitioning from imitation to innovation, with emergingBiotechRapid rise, but lacking self-production capacity, has led to a significant outsourcing of production operations. The identity of outsourcing service providers has gradually shifted from being sellers of services to those seeking gold; on the other hand, China's engineer dividend remains, and its labor cost advantage over overseas markets has also driven the focus of outsourcing services from overseas to China's industries.

Dr. Wang Xin pointed out, Chinese medical enterprisesTop 20The average total market value gap with US companies9Multiple times, and the total market value is more concentrated in leading enterprises, with a much lower market maturity compared to the United States. United StatesTop 20Enterprise market value average1,759.73billions, half of the enterprises are above the average, while in ChinaTop 20The average enterprise market value is only193.20billions of dollars, and only7Leading companies are above the average. In addition, China's top20The market value of the top enterprises is the sum3,864billion US dollars, still lower than UnitedHealth1Family-owned4,319Billions of dollars, multiple data points indicate that Chinese pharmaceutical companies are still focusing on the domestic market, with enormous growth potential ahead.

The data shows,2021The global equity financing scale has been steadily increasing, with the Chinese mainland consistently ranking second in recent two years. Affected byAThe promotion of the share registration system,2021Domestic for the yearIPO listingThe amount and number of funds raised have reached new highs, compared with Hong Kong stocksIPO listingThe market is more active.2021yearAshareIPO listingIn terms of financing scale, the top five industries are equipment manufacturing, information media, healthcare, energy and chemicals, and consumer goods. Among them, the healthcare industry910.7The financing scale of hundreds of millions ranks third.IPO listingIn terms of the number of enterprises, the healthcare industry ranks fifth.

Brief introductionAAfter discussing the current situation of the healthcare industry, Dr. Wang Xin focused on introducing Hong Kong stocks18AAnd the situation in the biotechnology field of the Sci-tech Innovation Board.

According to a study by Frost & Sullivan, biotech companies listed on the Sci-tech Innovation Board are mostly concentrated in the pharmaceutical sector. The vast majority of these companies focus on the research and development and production of oncology drugs, autoimmune disease drugs, and metabolic system diseases drugs. Among the biotech enterprises with a high market value, there are many that specialize in oncology drug research and development. In the Hong Kong stock market18ABiotech companies in pharmaceuticals, medical devices, andAIThe company covers all three major medical fields, with a focus on biopharmaceuticals in the pharmaceutical sector. Medical device companies are concentrated in three sub-sectors: in vitro diagnostics, medical equipment, and medical consumables.

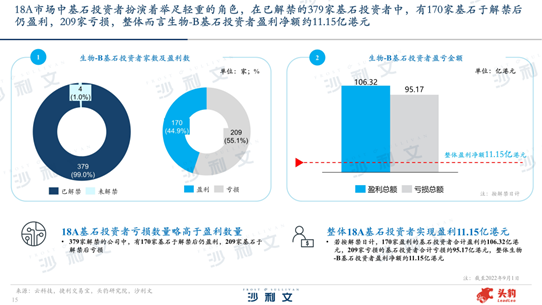

18AThe cornerstone investors in the market play a pivotal role, according to TradeGo.APPFundamentals investors data, for those that have been unlocked379Among the cornerstone investors, there are170Homefund, which remains profitable after the lifting of the ban,209Home Basic lost money after the lifting of the ban. If calculated based on the date of lifting the ban,170The total profit of cornerstone investors contributing to the company's profitability is approximately106.32HK$10 billion,209The combined losses of cornerstone investors with losses at home are about95.17HK$10 billion, overall biology-BNet profit of cornerstone investors is about11.15HK$10 billion.

Dr. Wang Xin pointed out that the overall market value of biotech companies is showing a downward trend. Data shows that the total issued market value of all biotech companies listed on the Hong Kong stock market is about7,283.6HK$10 billion, with the current total market value about4,574.9HK$10 billion, with the overall market value declining37.2%.At the same time, since2021year7Since the beginning of this month, the total number of subscribers to biotech companies has also shown a downward trend. On the other hand, there is a polarized change in the market value of biotech companies. The current market value of BGI HealthTech has increased compared to its initial offering market value.175.3%On the contrary, the current market value of Harvest Biotech has declined92.3%.

Recently, Hong Kong stocks rebounded, and pharmaceutical stocks continued to surge. Among biotech stocks, Cobi Pharma rose more than21%Rongchang Biotech surges19%Gensrite Biotechnology surges12%Nuo Cheng Jianhua and Yasheng Medicine rose more than11%Baiji Shenzhou, Fuhong Hansen, and others followed the trend up. Dr. Wang Xin stated that although the current valuation of the pharmaceutical sector is still at a low level over the past decade, and the institutional allocation ratio is also at a low level, there have been frequent favorable domestic policies recently, with significant marginal improvements in policies. Market sentiment is expected to continue to recover, and investment opportunities in the pharmaceutical sector are still favored.

Looking at the entire Hong Kong stock market18AMarket, according to Frost & Sullivan Jely(shenzhen)Cloud technology data shows,2022Looking at the price changes from the lowest price this year to now, biotech-BOverall increase of about34.54%, increase or decrease in priceTop 15The overall enterprise price rose by about54.83%The rebound strength is still acceptable; looking at the cumulative rise and fall data since listing, biotech-BOverall decline37.33%IncreaseTop 15The overall stock market fell28.4%.

"Benefiting from industry characteristics and market environment, the healthcare sector has broad development opportunities in the medium to long term. In the face of short-term fluctuations, biotech companies need new investment for empowerment and support," said Dr. Wang Xin.

In the face of the current market environment and challenges, new investment will become the development direction for biotech companies' investment and financing. What is new investment? Dr. Wang Xin further explained that new investment is a brand-new investment concept and methodology, a three-dimensional, multi-dimensional spatial point matrix service system. New investment shoulders the mission of 'three endowments', namely endowing enterprise capital operations with value, industry transformation and upgrading with energy, and national economic development with services.

Frost & Sullivan, together with representatives from various sectors, has jointly launched a three-dimensional, multi-dimensional spatial point cloud-based service system..."TIM(Total Investment Management), namely 'All-region Investment Management', is different from the classic investment model of 'fundraising, investment, management, and exit' in the past. All-region Investment Management is committed to creating an ecological service system covering the entire life cycle and industrial chain of enterprises. It integrates a series of service capabilities through internalization and linkage within the system, including enterprise management, regulatory communication, industry development trend analysis, market and strategic planning, brand value empowerment, etc., to provide enterprises with better investment management services in all aspects.

Frost & Sullivan and LeadLeo have nearly500The human analyst team at Frost & Sullivan has long been committed to in-depth industry and corporate original research. Frost & Sullivan has a global presence of over60The annually accumulated industry-wide database, reported by LeadLeo and included in the databases of one of the world's largest financial market data and infrastructure providers, Refinitiv, enables precise reachability of reports.190country4More than 10,000 institutions,40For users of the Ten-thousand-Dollar Professional Finance platform, seamless integration is available, building a bridge between both the supply and demand sides of investment and financing.

Dr. Wang Xin pointed out that achieving growth is the top priority for the development of biotech companies, while innovation and entrepreneurship are the core driving forces for their development. Becoming a market leader is a lofty goal for the long-term sustainability of a company's foundation.

"New investments" refer to those made in companies that have already achieved growth, or are expected to demonstrate growth, innovation, and leadership in the future. Frost & Sullivan aims to integrate professional resources, a pool of high-quality targets, capital, growth and R&D experts, and deeply empower practitioners of 'new investments' in the biotechnology field. Help biotech companies achieve growth, empower the transformation and upgrading of the biotech industry through innovation and technology development, cultivate leading Chinese entrepreneurs, and ultimately promote China's economic and social development.