On the afternoon of November 27th, KPMG held the 'Hong Kong Capital Market Seminar' in Shanghai. The seminar was themed 'The Wind of Change Ahead: How Can Enterprises Rekindle Successful Issuances?' It invited guests from Frost & Sullivan (Frost & Sullivan, abbreviated as 'Frost & Sullivan'), Ping An Securities, and Jintiancheng Law Firm to share and exchange views with representatives of enterprises interested in listing in Hong Kong on dimensions such as Hong Kong capital market dynamics, relevant listing preparations, and business opportunities and challenges amidst consumer recovery.

The meeting was chaired by Ms. Feng Yijia, Capital Markets Partner of KPMG China East and West. Mr. Fang Haijie, Capital Markets Partner of KPMG China East and West, delivered an opening speech, expressing gratitude to all parties for their support to KPMG and expressing the hope that in the future KPMG could better collaborate with various intermediary institutions to jointly assist enterprises planning to go public in Hong Kong.

Mr. Zhu Yiming, Executive Director of Frost & Sullivan Greater China, was invited to attend the seminar and delivered a speech titled "Crossing Cycles: Insights into Business Opportunities and Challenges in the Recovery of Consumption". He looked ahead to China's consumer market and future new growth points, shared his outlook on the Chinese consumer market with the guests, as well as his insights into opportunities and challenges.

Zhu Yiming, Executive Director of Frost & Sullivan Greater China

Zhu Yiming pointed out that the consumer industry is positively correlated with the development of the national economy. For the Chinese economy, the twenty years from 2000 to 2020 were of extraordinary significance, marking an important leap from 'catching up' to 'leading'. Around 2000, the development of the Chinese economy was relatively lagging behind, with a per capita GDP of only about $900. With the deepening of reform and opening up and China's accession to the World Trade Organization (WTO), the Chinese economy officially entered a period of rapid development. By 2020, China had become an important force in global economic development, with its total economic volume growing from $1.2 trillion to $14.7 trillion, and its per capita GDP also increasing to over $10,000. The compound growth rate over the past twenty years was 13%, making it the fastest-growing large-scale economy globally.

At the same time, China is the world's largest trading nation, with its scale of attracting foreign investment consistently ranking second globally. Globalization has driven China's development, and China's growth has injected strong momentum into the global economy. With the rapid growth and structural upgrading of the Chinese economy, China's industrial structure has gradually transformed. Traditional industries have slowly faded from the historical stage, while emerging industries have risen rapidly. However, no matter how changes occur, the consumer industry remains one of the pillar industries of the Chinese economy.

"There are three carriages that pull the economy forward: exports, investment, and consumption," Zhu Yiming further explained. In the past, China mainly relied on exports and investment, while the United States relied on consumption. However, China has now entered a critical stage of transitioning from high-speed growth to high-quality development. The central government has proposed the "dual circulation" strategy, emphasizing the expansion of domestic demand and encouraging consumption. At the same time, under the backdrop of common prosperity and driven by the continuous increase in disposable income among residents, the consumer industry is undoubtedly an important growth engine for China's economy in the future.

According to data from the National Bureau of Statistics, China's total retail sales of consumer goods in 2022 reached 44 trillion yuan, making it the world's second-largest consumer market, accounting for about 95% of the US market. Currently, there is still a significant gap between China's per capita consumption expenditure and that of developed countries such as the United States. According to World Bank data, the per capita final consumption of residents in the United States reached $42,000, ranking first, while European developed countries such as the UK, Germany, and France have all reached over $20,000. Japan, which is close to China, has also achieved a per capita expenditure level of $19,000, compared to China's only $4,400, which is about one-tenth of that of the US.

Zhu Yiming stated that China's economic development has continuously narrowed the per capita expenditure gap between China and the United States. In the foreseeable future, China will become the world's largest consumer market. The consumer base of China's 1.4 billion people will unleash tremendous consumption potential in the future, continuously leading the global consumption process.

Looking ahead, China will, like all developed countries in history, enter a consumption-driven development phase after per capita GDP exceeds $10,000.At this stage, people's quality requirements for basic survival-oriented (such as clothing, food, shelter, and transportation) consumption will increase. Development-oriented (such as education and healthcare) and enjoyment-oriented (such as entertainment) consumption will grow, and the proportion of service consumption will further expand. Against this backdrop, people place more emphasis on quality and experience than price.

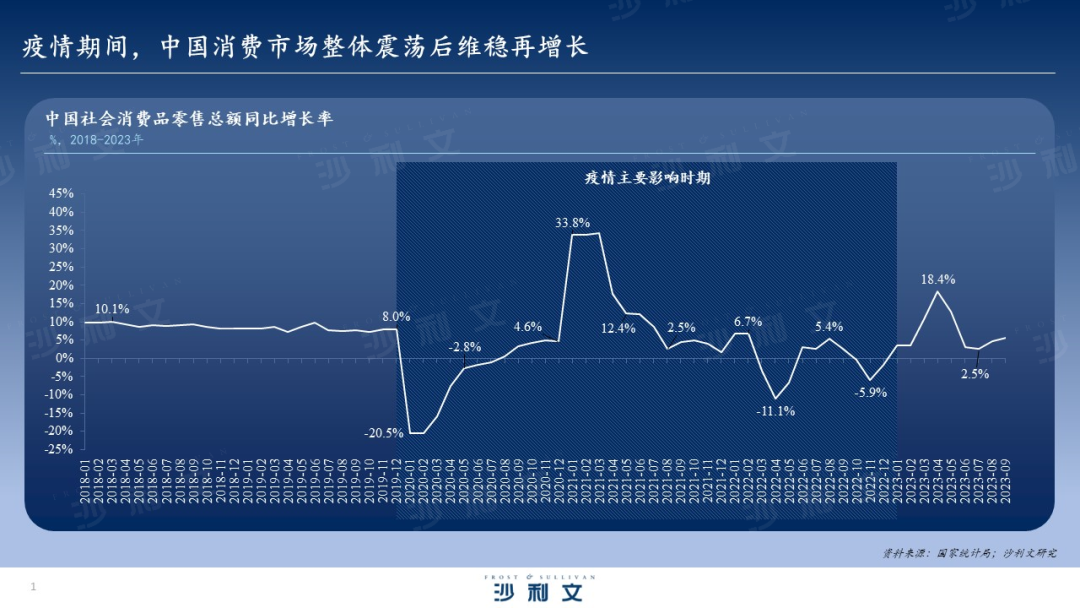

Subsequently, Zhu Yiming summarized the development of China's consumer industry over the past three years and looked ahead to the development trends in the post-pandemic era. From 2020 to 2022, final consumption expenditure accounted for more than 50% of GDP on average, exceeding 60 trillion yuan in 2022, contributing 32.8% to China's economic growth and driving an increase of 1.0 percentage points in economic growth. Although the scale of China's consumer market growth was impacted and fluctuated between 2020 and 2022, it still demonstrated strong resilience overall.

"Publicly known, the years from 2020 to 2022 are undoubtedly of special significance for both China and the global consumer market. Over these more than three years, China's consumer industry has experienced many significant changes in the development environment, generally showing a pattern of stabilizing after shocks and then resuming growth."Zhu Yiming further added that in 2020, the outbreak of the COVID-19 pandemic and epidemic prevention and control policies led to a general reduction in residents' outings, severely affecting the consumer market. The total retail sales of consumer goods dropped significantly year-on-year compared to historical years. However, this trend improved after the control of the epidemic in various regions in 2021, with consumption beginning to warm up. The recurrence of the epidemic in many places at the end of the year caused short-term disturbances to the consumer market. By 2022, China's overall consumption situation was affected by factors such as local-scale rebounds in domestic epidemics, rising unemployment rates, and reduced consumer willingness, showing an abrupt decline followed by a slow recovery and then tending towards stability.

The consumption concepts, models and habits of Chinese residents are quietly changing. According to a Frost & Sullivan study, the development trend of consumer spending during the pandemic era shows the following characteristics:

(1) The consumption structure of residents is continuously optimizing and upgrading

Since 2020, although there have been short-term fluctuations in the consumption structure of Chinese residents, the overall trend has remained towards upgrading towards quality-oriented consumption. Whether in the areas of bulk commodity consumption such as housing and transportation, or in emerging service consumption areas like culture, health, and entertainment, residents' preference for high-quality and diversified products and services is becoming increasingly evident. It is expected that in the post-pandemic era, Chinese residents' consumption will resume its trend of structural upgrading.

Since the outbreak of the pandemic, new business forms such as online shopping and internet+ services have become new anchors driving domestic demand. Before 2020, China's online retail industry had already developed far ahead globally. From 2013 to 2022, China maintained its position as the world's largest online retail market for 10 consecutive years, and this leading advantage was further expanded after the pandemic. Under the impact of the pandemic, online consumption effectively drove resilient growth in consumption. Online retail has become the main consumption channel for Chinese consumers. As of December 2022, the number of internet users in China reached 1.067 billion, with online shopping users accounting for 79.2%.

Looking at the segmented markets, live streaming e-commerce, social e-commerce, and short video e-commerce have developed rapidly over these three years. To some extent, they have not only met people's consumption needs for purchasing goods and services but also leisure and entertainment. Watching live broadcasts while consuming and browsing short videos while shopping have become consumption habits for more people. As of December 2022, the scale of online live streaming users, instant messaging users, and short video users in China reached 751 million, 1.038 billion, and 1.012 billion respectively, accounting for 70.3%, 97.2%, and 94.8% of internet users. This shows the high penetration of instant messaging and short videos, as well as the growth potential of live streaming users.

In addition, Frost & Sullivan has observed that 'Internet + services' are becoming a new space for consumer recovery growth. Online service consumption has somewhat compensated for the slowdown in contact-based consumption. For example, in the field of online healthcare, there are currently over 3,000 internet hospitals nationwide, with remote medical service coverage reaching 100% in counties (cities, districts); in cultural and entertainment, cloud tourism, cloud drama watching, cloud exhibition viewing, etc., have become new consumer trends.

(3) Domestic consumption continues to rise

With the improvement in quality and upgrade of consumption, more consumers are paying attention to the value and cultural attributes of products themselves, and their recognition of some domestic brands is continuously increasing. The consumption of domestic products, represented by new national brands, has risen comprehensively.

In 2022, the number of domestic brand products on Douyin increased by 508% year-on-year, with domestic brands accounting for 92% of the hot search list items. The rise in domestic consumption is also closely related to the emergence of the new generation represented by millennials and Generation Z. Surveys show that Chinese netizens recognize domestic products at an approval rate of 82.4%, with younger generations such as 'post-90s' and 'post-00s' choosing to support domestic products at a rate exceeding 90%. In the consumption of national trend brands across the industry, the new generation has contributed 74% to national trend consumption, becoming the absolute main force.

During the pandemic, people's demand for green and healthy lifestyles has also increased. Consumers are not only concerned about the quality of products and services but also pay attention to the integrated development of consumption and environmental protection. Green consumption has shown rapid popularization. Data shows that in 2020, the proportion of people who could regularly purchase green products was 30 to 40%, and by 2022, this proportion had exceeded 60%, and it will continue to rise in 2023 and beyond. Nowadays, green consumption methods have been widely recognized in consumer areas such as food, clothing, housing, transportation, usage, and tourism.

Zhu Yiming stated that in 2022, China is at the height of personalized consumption and the era of Chinese culture.Looking back at the development history of the United States and Japan, after the era of personalized consumption, a new consumption era is about to arrive. However, the themes of the new consumption era in the United States and Japan are quite different: the theme in the United States is the rise of new consumption habits and new consumption propositions that have brought about a large number of new demands, based on the opportunities for new brand emergence (such as Anthropologie, lululemon, etc.); the theme in Japan is low desire, a pursuit of simplicity, craftsmanship, practicality, and de-branding, which has led to better growth momentum for Uniqlo and Misfit.

The new era consumption themes in the United States and Japan are two completely opposite directions. So what will happen to China's consumer industry? Frost & Sullivan believes that China's consumer industry will embark on its own path, and in the future, there will be two levels of differentiation in development.Regarding the overall direction of future consumer investment in China, Frost & Sullivan has summarized the following consumption trends: 1) Luxury goods possess long-term value; 2) Consumer goods with strong brand and functionality are more competitive; 3) In service consumption, industries that can achieve chain operation and standardization are good investment directions; 4) Investment opportunities in channels and mass consumer goods mainly come from business expansion.